Review and comparison of the Federal & Quebec Mandatory Disclosure Rules

Prepared by Danny Guérin, Omar Yassine and Shant Ghazelian, Andersen in Montreal (Canada)

In the dynamic landscape of modernized society, many systems crucially hinge on robust legal regulations to ensure a smooth flow of continuity. Central to this is the Canadian Tax System, a cornerstone underpinned by the Income Tax Act[1] (hereafter the “ITA”). The ITA has seen many amendments throughout the years and is in constant evolution due, in part, to the evolution of societal and economic needs, and in part, to taxpayers’ continued ability to take advantage of breaches in the tax legislation. Understandably so, this reality has posed significant challenges for the Canada Revenue Agency (“CRA”), which has endeavored, though not always successfully, to try and bridge the gaps. For these very reasons, the mandatory disclosure rules (hereafter the “MDRs”) were introduced in the late 2000s to minimize as much as possible crucial information going unnoticed by mandating the disclosure of certain transactions.

It is interesting to note that the Canadian MDRs were recently amended to align with the Organisation for Economic Co-operation and Development (“OECD”) recommendations. In this context, it is relevant to review the application of the MDRs and the changes made to these rules to broaden their application and to make them more punitive.

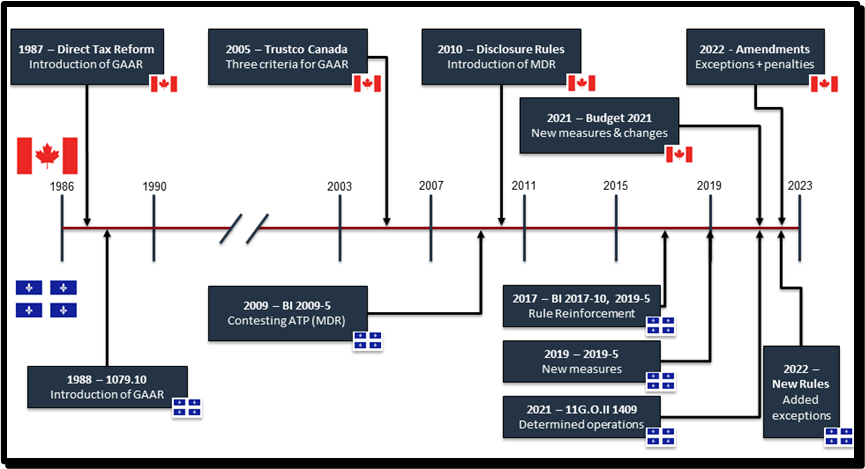

Evolution of the MDRs over the years

The below table shows that the MDRs have evolved greatly over the years, and that Revenu Québec has often been a step ahead of the CRA. Please note that the purpose of this publication is not to make a comprehensive historical review of the MDRs, but rather to discuss the current application of these rules.

THE MANDATORY DISCLOSURE RULES – A FEDERAL OVERVIEW

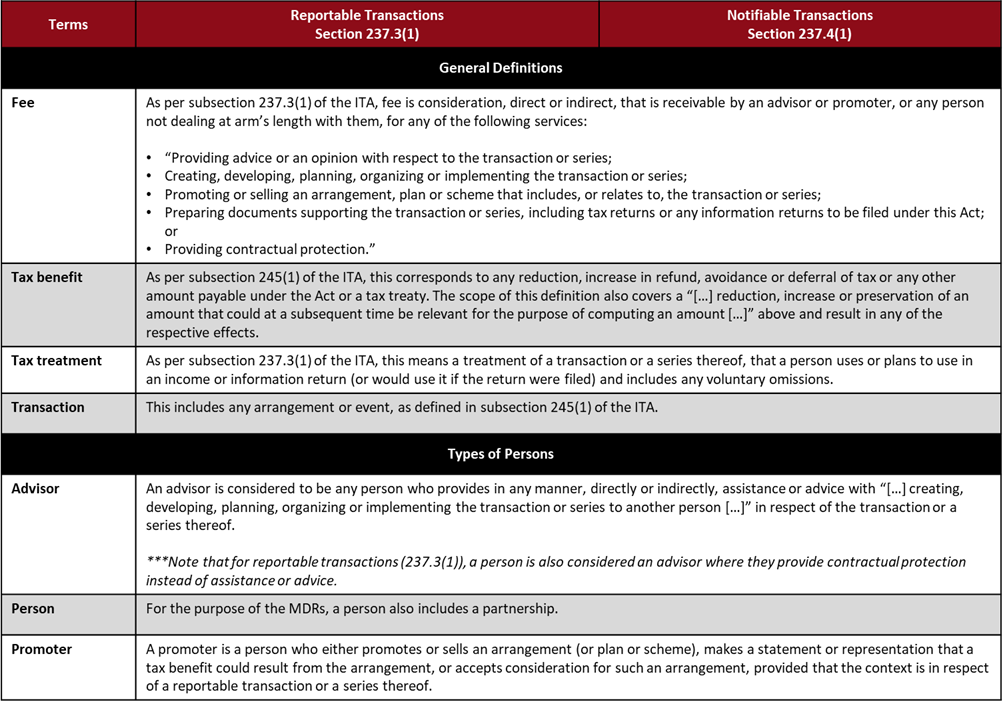

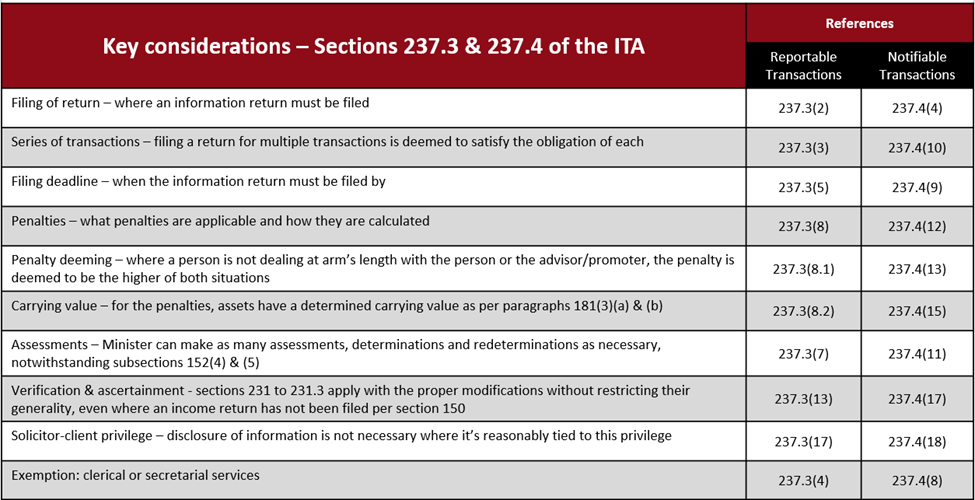

Prior to diving into the details of the MDRs, it is recommended to take note of the table below containing all relevant common definitions assigned to reportable transactions per section 237.3 of the ITA and to notifiable transactions per section 237.4 of the ITA.

As indicated above, the definitions pertinent to sections 237.3 and 237.4 of the ITA are quite broad in the sense that many transactions can be captured, including transactions made for bona fide commercial reasons. The meanings assigned to advisors or promoters are also quite large and reach beyond the scope of their job titles for the purposes of the Canadian MDRs.

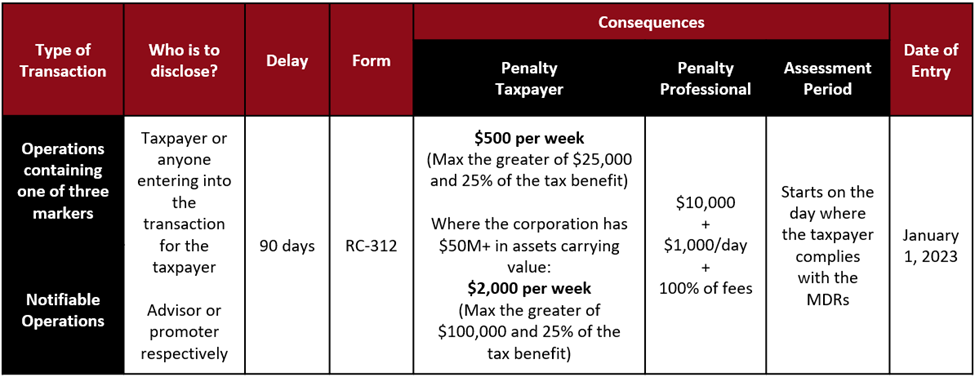

Under the MDRs, a transaction needs to meet the conditions below to qualify as a reportable transaction.

- The transaction must be an avoidance transaction.

- One the 3 below markers needs to be met:

- Conditional fees.

- Confidential protection.

- Contractual protection.

To understand the meaning of a reportable transaction, it is important to note that an avoidance transaction is defined as “a transaction or a series of transactions which includes the former, where one of the main purposes is to obtain a tax benefit”[2]. As discussed previously, this definition is very broad, and could therefore include bona fide transactions. For example, a transaction that is concluded for commercial purposes could be considered an avoidance transaction simply because a significant tax benefit arises as a result.

Furthermore, for an avoidance transaction to be considered as reportable transaction, it must meet one of the following 3 markers:

It is to be noted that standard professional liability insurance is not considered to be contractual protection, along with any aspect that is integral to a business purchase or transfer agreement so long as said protection is undertaken to ensure the fidelity and exactitude of the purchase price and is not primarily obtained for tax benefit purposes. Note that any of the markers can be either direct or indirect, immediate or future, and absolute or contingent.

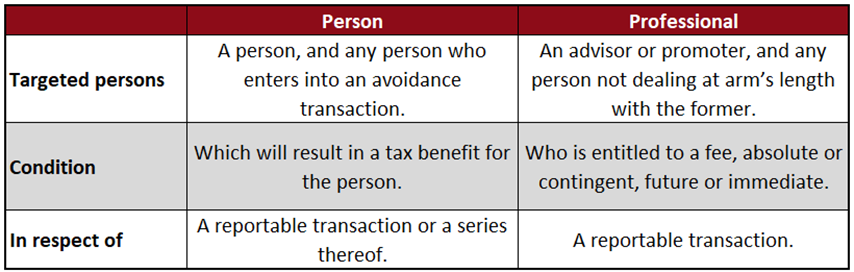

As per subsection 237.3(2) of the ITA, an information return known as form RC312 is to be filed with the Minister concerning reportable transactions by four distinct types of persons. The target demographic can be simplified and grouped into pairs as follows:

As per subsection 237.3(4) of the ITA, an exception exists that exempts a person from filing a form with the Minister concerning a reportable transaction where the person entered such a transaction solely to provide clerical or secretarial services. Disclosure of information that is reasonably targeted by solicitor-client privilege is also not required[3].

Subsection 237.3(13) of the ITA also provides that the verification or ascertainment capabilities of the Minister concerning information relating to a reportable transaction is not limited by the generalities of sections 231 to 231.3, even if an income return has not been filed by a taxpayer[4].

Where a person is required to file a prescribed form with the Minister, the filing deadline can vary whether the filer is the person in question, or the respective advisor or promoter (or any persons not dealing at arm’s length, respectively).

- For a person obtaining the tax benefit, or a person not dealing at arm’s length that has entered into the transaction for the benefit of the former, the information return is to be filed within 90 days after the earliest of the following days:

- The day where a contractual obligation exists to enter into the reportable transaction, and

- The day where the reportable transaction is undertaken or entered into.

- For an advisor or promoter, or a person not dealing at arm’s length with the formers, the information return is to be filed on the earliest (and not within 90 days) day described above.

Where each transaction of the series in question is a reportable transaction for which a prescribed form must be filed, a person can file a single form containing all the necessary information concerning all the transactions of the series. In this case, as per subsection 237.3(3) of the ITA, the person is deemed to have satisfied all the obligations for the MDRs.

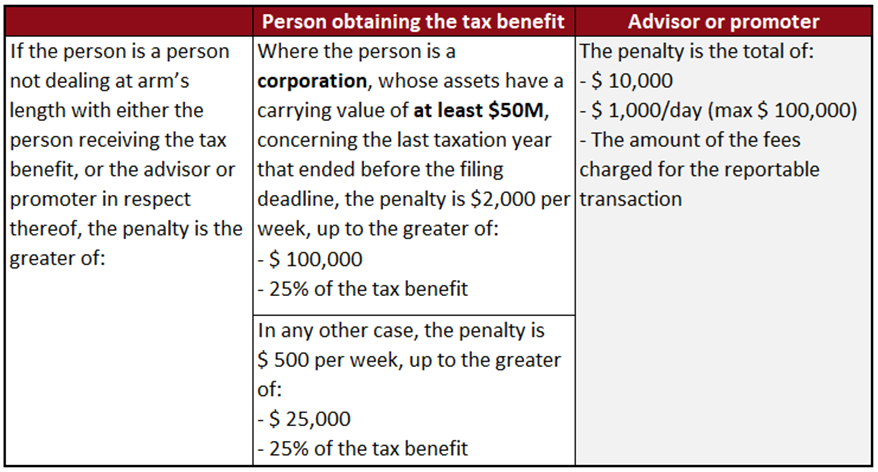

Failure to comply with the MDRs entails significant penalties. With the purpose of discouraging such behaviour, the following penalties, on a cumulative basis so long as the failure continues, are applicable to the respective persons starting the day after the filing deadline.

It is to be noted that subsection 237.3(7) of the ITA gives the Minister the power to make any assessments, determinations, and redeterminations necessary to aid in the application of the penalties, regardless of the constraints provided by subsections 152(4) and (5) of the ITA concerning assessments.

A due diligence exception also exists under subsection 237.3(11) “[…] if the person has exercised the degree of care, diligence and skill to prevent the failure to file that a reasonably prudent person would have exercised in comparable circumstances.” This exception avoids the penalty liability but does not waive the obligation to file.

Subsection 245(2) of the ITA, more popularly known as the application of the GAAR, is limited by subsection 245(4) of the ITA which deems the GAAR applicable to a transaction only where it is reasonable to consider it to be, directly or indirectly, a misuse or an abuse of the provisions of the ITA, or any other enactment relating to computing income tax.

The MDRs have a provision under subsection 237.3(6) of the ITA to bypass the narrowing agent that is subsection 245(4) of the ITA, and thus widening the GAAR’s range of application in cases where such transaction would meet the avoidance transaction definition contained under subsection 245(3) of the ITA, when the following three conditions are met:

- The obligation to file an information return in respect of a reportable transaction, or a series thereof, has not been satisfied,

- A person is liable to a penalty in respect of the reportable transaction or a series thereof,

- The penalty applicable or interest therein has not been paid or has triggered a refund or a credit[5].

This means that failure to file and failure to pay the respective interest and penalties results in the tax benefit being denied, as would be the case where the GAAR would apply. Consequently, where the penalties and interest amounts are fully paid, the Minister may allow the denied tax benefit. This will depend on the CRA’s analysis of whether the transaction in question is targeted by GAAR, including subsection 245(4) of the ITA.

Notwithstanding the above-mentioned, an information return in respect of a reportable transaction is not considered as an admission of any of the following:

- Application of section 245 (GAAR),

- Any transaction is part of a series of transactions, and

- A tax benefit was derived from the transactions or series of transactions.

This liability waiver is provided by subsection 237.3(12) of the ITA for the purpose of enticing taxpayers to disclose their information as required without having to be wary of any potential consequences that may result.

As per subsection 237.4(1) of the ITA, notifiable transactions are transactions or series thereof that are the same or substantially similar to a “transaction that is designated at that time by the Minister under subsection (3)”. Below is the list of transactions that are currently designated as notifiable transactions:

- CCPC status manipulation to avoid tax on passive income,

- Use of a partnership to avoid the application of the “straddle” transactions rules found in subsections 18(17) to 18(23),

- Avoiding the 21-year rule of deemed disposition under subsection 104(4) or seeking to avoid rules contained in subsections 107(2.1) and 107(5),

- Manipulation of bankruptcy status to avoid the application of the debt forgiveness rules,

- Transactions that avoid the application of the limitation of tax attributes trading on an acquisition of control relying on the purpose tests of either 256.1(2)(d), 256.1(4)(a) or 256.1(6),

- Back-to-back loan arrangements using intermediaries to circumvent the application of the thin capitalization rules and Part XIII tax.

As per subsection 237.4(2) of the ITA, concerning notifiable transactions, “substantially similar” includes any transaction or series thereof where a person is expected to obtain the same or similar types of tax consequences, that is factually similar or based on a similar tax strategy. This term is also “[…] to be interpreted broadly in favour of disclosure.”

While not expressly discussed, it is to be noted that notifiable transactions under section 237.4 of the ITA have a near-exact treatment as the reportable transactions concerning the persons involved, filing requirements as well as penalties.

Differences between Notifiable transactions & Reportable Transactions

Due diligence exception

Concerning the due diligence exception, a person (not an advisor or a promoter) is exempt from this section “[…] if the person has exercised the degree of care, diligence and skill in determining whether the transaction is a notifiable transaction that a reasonably prudent person would have exercised in comparable circumstances” as per subsection 237.4(6) of the ITA.

This is different from the due diligence exception for reportable transactions under 237.3(11) in the sense that the taxpayer must have been diligent in determining the nature of the transaction and not in preventing failure to file. In addition, the due diligence exception for reportable transactions waives the penalty liability only, while subsection 237.4(6) of the ITA exempts the person from filing altogether in respect with notifiable transactions.

Other exceptions

It is important to note that all interrelations with GAAR are not applicable for notifiable transactions.

An exception exists for advisors or promoters not to be targeted where it’s not reasonable to expect the professional to know that the transaction was a notifiable transaction, as per subsection 237.4(7) of the ITA.

Not an admission

Where an information return is filed in respect of a notifiable transaction, as per subsection 237.4(16) of the ITA, the filing is not an admission by the person that any transaction is part of a series. As notifiable transactions are not necessarily tied to avoidance, there is no mention of the GAAR as opposed to the reportable transactions.

Other Particularities

As per subsection 237.4(5) of the ITA, where the advisor or promoter is an employer or partnership required to file an information return, the filing in prescribed form and manner is deemed to have been made by each employee or partner of the particular person in respect of the transaction. This measure exists to alleviate the administrative burden of the particular person and the other parties implicated. In tandem, subsection 237.4(14) of the ITA also provides that any person who is deemed to file an information return is not liable to a penalty.

THE MANDATORY DISCLOSURE RULES – A PROVINCIAL OVERVIEW

As previously introduced, the MDRs at the provincial level, referred to as “divulgations obligatoires”, are a set of numerous articles that have a broader application range than their federal equivalents. Six different articles specifically tailored to certain transactions are found in the Loi sur les Impôts[6] (hereafter “LI”).

Contrary to the ITA’s “marker presence” system, the three same markers are split up into three different articles. This bypasses the need to trigger one of the three markers as they are completely unique articles sharing a few similarities. In tandem, the remaining articles encompass designated operations, promotions of operations and nominee contracts respectively. The disclosure of information is detailed in article 1079.8.9 of the LI. Nominee contracts have a specific treatment that will be addressed subsequent to the general applications.

While most definitions carry over to the provincial level, an advisor, as per article 1079.8.1 of the LI, is a person (or partnership) who provides advice, assistance or any other type of help in the conception, implementation, commercialization or promotion of the operation. As per article 1079.9, a promoter is a person (or partnership) who meets the following conditions:

- Commercializes or promotes the transaction or series thereof, or supports its growth or interest,

- Receives or has the right to receive (or any related or associated person or partnership receives or has a right to receive), directly or indirectly, a fee for the above-mentioned, and

- Plays a pivotal role in the above-mentioned, as it’s reasonable to consider.

All of the following provincial MDRs are to be determined without reference to article 1079.9, i.e., the provincial GAAR, and can be undertaken either directly or indirectly.

As for the Federal MDRs[7], disclosure through an information return is necessary for any person or partnership that enters into the operations below:

- Conditional fees: An operation that contains a contingent renumeration, such as an amount paid to a professional on the condition that a tax benefit is obtained through the operation.

- Confidential protection: A confidential operation.

- Contractual protection: An operation providing contractual protection.

However, contrary to the CRA, RQ introduced a threshold of significance to trigger the “market presence” transactions. The thresholds are as follows:

- A $25,000 or greater tax benefit for the person, or

- A $100,000 shift in taxable income of the person or partnership.

As per article 1079.8.6.2 of the LI, the following operations are considered determined operations and will require a specific disclosure of information. Apart from obtaining relevant information to better study the market and taxpayers, RQ’s objective through these determined operations is to provide more accurate legislative amendments for the future, and to modify the behaviours of taxpayers by either discouraging an operation or by having an information return. Determined operations are published to the “Gazette officielle du Québec”. It is interesting to note that the CRA identified six notifiable transactions, while RQ only designated four transactions as determined transactions.

Avoidance of the deemed disposition of property rules in a trust

Article 653 of the LI oversees a deemed disposition of all property owned by a trust every 21 years to tax accrued gains. For anti-avoidance purposes, rollovers to prevent such a disposition are disallowed.

The CRA[8] is of the opinion that a distribution from a discretionary family trust to a Canadian corporation whose shares are owned by a new discretionary family trust (to reset the 21-year timer), is a planning that circumvents the anti-avoidance rule in subsection 104(5.8) of the ITA “in a manner that frustrates the object, spirit and purpose of that provision, the deemed disposition rule in paragraph 104(4)(b) and the scheme of the Act as a whole”[9].

In this case, disclosure is required by at least one of the two trusts involved in such an operation, but the responsibility falls on both concerning non-compliance. The trust agreement cannot alter such requirements. The disclosure is to be made no later than 60 days after the distribution of property by the trust.

Payments made to countries that do not have a tax treaty with Canada

Disclosure is only necessary in a context where a Quebec resident individual or partnership makes and deducts payments totalling at least $1,000,000 to a related party in a foreign jurisdiction with no tax treaty with Canada. The person who receives a deduction for these payments must disclose no later than the usual filing date of the person. No further inclusions or exclusions have been provided.

Multiplication of the Lifetime Capital Gains Exemption (LCGE)

Before 2017, taxpayers used to set up trusts with several beneficiaries to allocate to each of them the capital gain accumulated on the disposal of particular shares. Each beneficiary could then benefit from their LCGE on the part of the capital gain allocated to them to limit their taxation, and then redistribute the allocated payments to the taxpayer who had set up the trust. This type of planning was considered as a simulation for tax purposes and was shut down by the Tax Court of Canada[10] in 2017.

Similarly, the spouse of a shareholder can become a shareholder to multiply the LCGE claimed through manipulation of the “TOSI” rules (tax on split income). The Federal Court of Appeal was quick to rule against the taxpayers in 2018[11] for this specific type of situation.

Where the allocation of capital gains is legitimate, meaning that the persons who claimed their LCGE receive their payments and can use it without limitation, then the disclosure does not apply. Note that a legitimate operation followed by another transaction can be considered as part of the same series and get impacted by the GAAR if it was the taxpayer’s intent to plan such a series to multiply the LCGE before disposition.

Furthermore, it is interesting to note that taxpayers could have to disclose a transaction even if the transaction happens many years after the use of their LCGE. Indeed, the wording of the articles can target transactions where certain amounts or assets were to be exchanged (or gifted) between two parties, regardless of when the transaction happens[12].

The disclosure of this type of transaction is required by the individual claiming the LCGE, not the trust. The relevant information must be filed within 60 days after the latest of:

- The day of the alienation, and

- The day of the transfer or of the borrowing, concerning a multiplication through usage of a trust.

Business of tax attributes

Once an acquisition of control occurs, the law restricts the use of tax attributes of the acquiree, such as non-capital losses. This targets any use of tax benefits from another taxpayer unless both parties were related prior to the operations. This also targets tax attributes used by corporations or trusts following their capitalization by a third party.

In 2021, the Federal Court of Appeal has confirmed the GAAR’s application in a situation where a corporation circumvents an acquisition of control through an initial public offering (IPO) and thus is not disallowed to use the applicable losses[13].

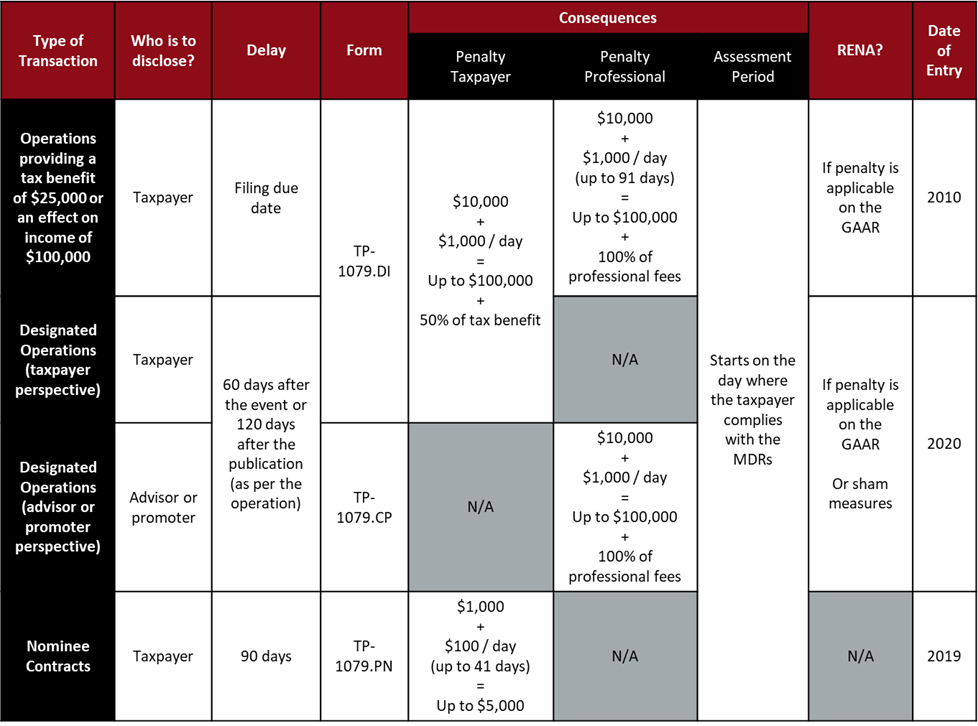

For the purposes of the provincial MDRs, a designated operation (“opérations désignées”) is an operation where its form and factual substance significantly align with those of the determined operations as per article 1079.8.6.2 of the LI.

An advisor or promoter executing the commercialization or promotion of a designated operation above entails separate disclosure requirements as per article 1079.8.6.3 of the LI. For this to be applicable, the operation must be published to the “Gazette officielle du Québec” and be void of any significant modification to its form and factual substance to adapt its potential application to different persons or partnerships.

Particularities of information to be disclosed

Marker-based operations and designated operations

For all the marker-based operations (operations tied to a contingent renumeration, confidential operations, operations providing contractual protection), as well as designated operations from the perspective of the taxpayer (not the advisor or promoter), form TP-1079.DI must be filed to the Minister, as per article 1079.8.9, containing all the following information:

- The identity of all parties implicated in the operation along with their ties within each other up to the realization of the operation;

- An exhaustive description of the operation-related facts;

- A presentation of all tax consequences that arise due to the operation; and

- Any other relevant information as demanded in the form.

As per article 1079.8.10, the filing deadline for the marker-based operations corresponds to the filing deadline of the person in question. In the case of partnerships, it is to be filed no later than the fiscal period filing deadline of the return.

As per article 1079.8.10.1 of the LI, the filing deadline for the information returns concerning the designated operations (from the taxpayer’s perspective) is the latest of the following:

- The 60th day following the day where the obligation to divulge is applicable, determined by the Minister,

- The 120th day following the designated operation’s publication in the “Gazette officielle du Québec”.

Failure to comply to the above-mentioned operations (marker-based and designated operations for the taxpayer) will trigger penalties amounting to:

- $10,000,

- $1,000 per late day up to 91 days, and

- 50% of the tax benefit (or 100% of the professional fees for an advisor or promoter).

Determined operations for advisors and promoters

As per articles 1079.8.9 and 1079.8.10.2 of the LI, regarding commercialization or promotion of determined operations, from the perspective of the advisor or promoter, form TP-1079.CP is to be filed no later than the latest of:

- The day that is 60 days following the day provided by the Regulation (variable depending on the planning), or

- The day that is 120 days following the transactions’ publication in the “Gazette officielle du Québec”.

Failure to comply will trigger penalties amounting to:

- $10,000,

- $1,000 per late day up to 91 days, and

- 100% of the professional fees in the case of an advisor or promoter.

This form contains an exhaustive description of the relative facts of the operation as well as any other information required, thus disclosing less information and preserving a client’s anonymity.

Where a person or a partnership embarks onto a nominee contract, where an operator acts on behalf of another person’s name, the person or partnership’s representatives must divulge the following information to the Minister through the form TP-1079.PN. The scope of this type of operation can have significant considerations for industries such as real estate, where an agent acting on behalf of a taxpayer is common. For these reasons, it’s important for people to be aware of the existence of these laws as to avoid penalties for non-disclosure. The form is to be filed no later than the 90th day following the conclusion of the contract:

- The effective date of the coming into force of the nominee contract;

- The identity of all relevant parties under the nominee contract;

- An exhaustive description of the relevant facts tied to the operation, detailed enough to allow the Minister to analyze and comprehensively understand the proper tax implications;

- The identity of any party that is affected by tax implications; and

- Any other relevant information demanded as per the form.

Failure to comply will trigger penalties amounting to (up to a maximum $5,000):

- $1,000, and

- $100 per late day up to 41 days.

The following table summarizes the Federal MDRs key information (excluding the UTP):

The following table summarizes the Québec MDRs key information (excluding the UTP and other non-mandatory disclosures):

DIFFERENCES BETWEEN FEDERAL AND PROVINCIAL

Certain important discrepancies remain for the MDRs at the federal and provincial levels. For instance, the breadth of the terms “advisor” and “promoter” are much less precise and thus more inclusive at the federal level. An advisor does not need to be promoting the operation in the ITA, whereas this is a requirement in the LI.

While the penalties are practically equal, the federal reporting deadlines are less forgiving. In parallel, the absence of a tax benefit or an income movement threshold at the federal widens the scope of the disclosure rules.

However, Quebec also mandates the disclosure of nominee contracts, a subject that is not discussed at the federal level. Preventive disclosures are also offered at the provincial level, probably targeted to taxpayers that do not want to absorb the risk of getting disallowed to enter into public mandates (RENA).

Finally, there are six notifiable transactions as per the ITA, whereas only four designated operations exist as per the LI.

Tax systems will always strive to be as fair, neutral, simple and equitable as possible. However, as the ITA pulls towards fairness and equity, it strays further and further from neutrality and simplicity. The MDRs are a means of obtaining information from taxpayers on certain transactions and penalizes those who do not comply. Moreover, it serves as a tool to strike fear in the hearts of taxpayers and professionals who may become hesitant to undertake a particular transaction that comes with the obligation of disclosing it.

While this may seem obvious, in the sense that everyone should just disclose the information as to avoid the potential liability, a problem arises with taxpayers who are unaware of such mandatory rules, notwithstanding the extensive administrative burden to be bestowed upon the CRA.

For professionals, big corporations, and other persons who are capable of understanding and interpreting the ITA, there are far more taxpayers left in the dark who are unaware of such rules, who do not have the financial means of seeking professional help, or simply do not have that reflex.

As the legislation is in constant adaptive evolution, how many more amendments are necessary to reach an equilibrium, where the legislator and the taxpayers are conjointly satisfied? It seems modernization has pushed us to require as much information as possible by force of law with the fair obsession to counter aggressive tax plannings undertaken by a small fraction of taxpayers, punishing those unaware of such measures and thus being defenseless under the complex array of tax laws that are the MDRs.

[1] Income Tax Act (R.S.C., 1985, c. 1 (5th Supp.))

[2] Subsection 237.3(1) of the ITA

[3] As per subsection 237.3(17) of the ITA.

[4] As per section 150 of the ITA.

[5] As determined under subsections 164(1.1) and (2) of the ITA respectively.

[6] Loi sur les Impôts, RLRQ c I-3, Partie 2

[7] Subsection 237.3(2) of the ITA.

[8] Technical Interpretation 2016-0669301C6, 2016 CTF Annual Conference, CRA Roundtable.

[9] Technical Interpretations 2017-0693321C6, STEP CRA Roundtable – June 13, 2017.

[10] Daniel Laplante v. Her Majesty the Queen, 2017 TCC 118.

[11] Guy Gervais v. Her Majesty the Queen, 2018 FCA 3.

[12] Revenu Québec has answered some questions regarding the breadth of these operations: https://cdn.ca.yapla.com/company/CPYYMDxL3sY6C1RHmn3wfAAq/asset/files/Programmes%20PDF/20230309_Programme_Colloque_reorganisations_entreprises_transactions_commerciales.pdf

[13] Her Majesty the Queen v. Deans Knight Income Corporation, 2021 FCA 160.