The View from Ottawa in One Chart — And What It Means for Your Tax Strategy

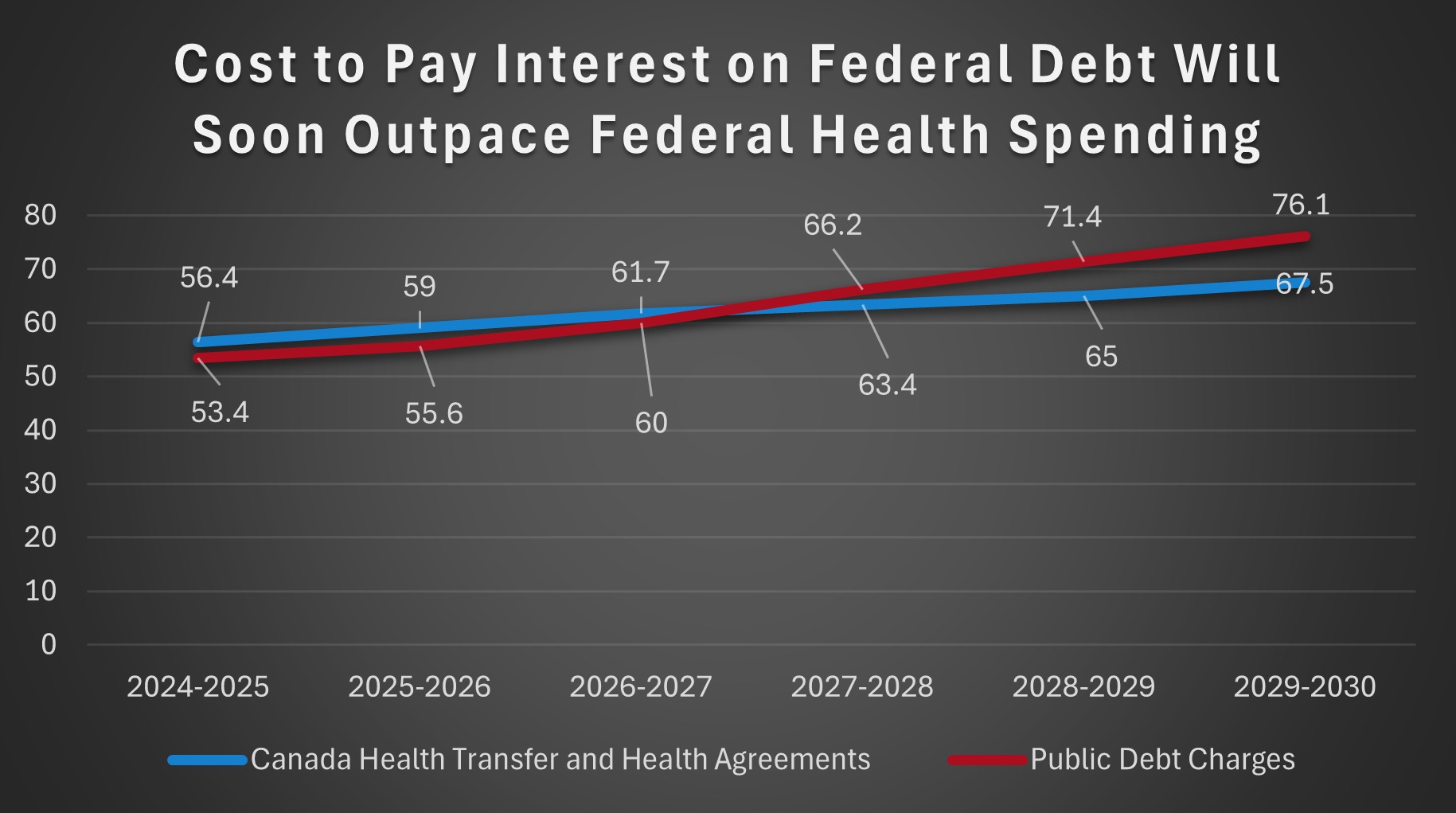

The chart above, using figures from federal Budget 2025, shows public debt charges rising steadily over the next several years and on track to overtake the combined cost of federal health transfers and health agreement payments by the end of the decade.

Budget 2025 also projects total federal tax revenue rising by 15.14%, from $416.7 billion to $479.8 billion, over the same period that public debt charges are expected to grow by 42.5%. When the cost of servicing government debt grows almost three times faster than the tax base, the implications for taxpayers are not abstract, they are operational.

For individuals, business owners and investors this divergence signals a future tax environment where governments are under sustained pressure to protect revenue, limit taxpayer’s flexibility, and scrutinize planning more closely. This is precisely the environment in which proactive, well-documented tax planning becomes essential.

Interest is Ottawa’s least flexible expense, and one of the most likely to result in pressure on taxpayers

Debt servicing costs are among the least flexible line items in the federal budget. Once debt is incurred, servicing costs cannot be reduced through policy announcements or legislative tweaks. As interest consumes a larger share of federal spending, fiscal pressure inevitably shifts elsewhere, often to the tax system.

For taxpayers, this translates into a higher likelihood of:

- Bracket creep and base-broadening measures

- Tighter rules around deductions, credits, and loss utilization

- Increased audit activity and enforcement

- Greater emphasis on compliance, documentation, and valuation support

From a tax advisory perspective, this reinforces the importance of forward-looking tax modelling, entity structuring, and defensive planning. Businesses that understand how cash flow, capital investments, and financing decisions interact with evolving tax rules are better positioned to absorb change without disruption.

The View from Ottawa: Why Tax Planning Is Becoming Less Optional

When interest on the federal debt begins to rival core social transfers, tax policy becomes driven less by political preference and more by fiscal arithmetic. And arithmetic is rarely negotiable.

In this environment, effective tax advisory services focus on:

- Optimizing after-tax cash flow through timing and structural planning

- Evaluating investment decisions under multiple tax-rate and incentive scenarios

- Managing risk through compliance reviews, audit readiness, and documentation

- Adapting ownership and financing structures as tax policy tightens

The takeaway for you is straightforward. As Ottawa’s fiscal flexibility narrows, taxpayer flexibility narrows with it. Businesses and individuals that plan early, model scenarios, and stay ahead of policy shifts will have more options than those reacting after changes are announced.

This is no longer just about minimizing tax—it is about building resilience into financial and business decisions in a more constrained fiscal environment.

If you would like to discuss your tax planning with our team, please contact Elan Harper below:

| Elan Harper, LLM (Tax), MBA, TEP Director, Andersen LLP |