Overview

On March 25th, 2025, the Saskatchewan government announced changes to its provincial tax laws in its budget 2025 Delivering for You. This comprehensive summary highlights the key changes that will influence the provincial tax environment in the coming years.

Personal Income Tax Measures

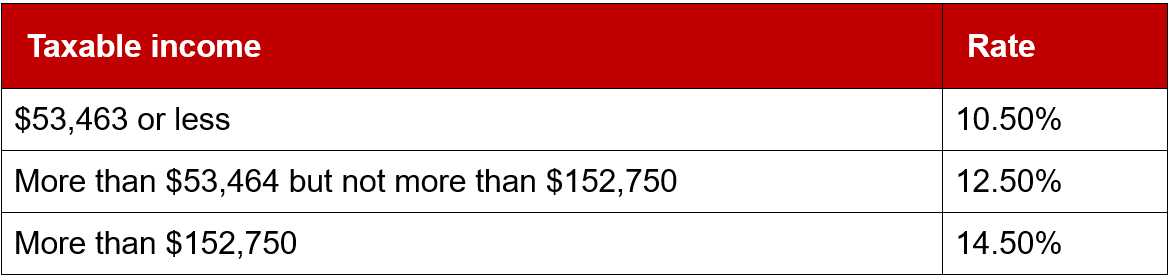

The budget introduces no change to the personal income tax rates. The income tax rates for the 2025 taxation year, based on your taxable income, are as follows:

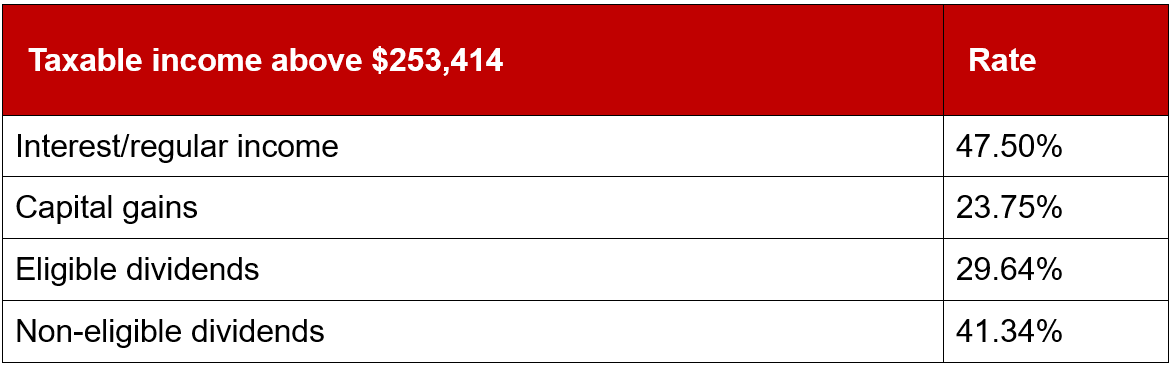

The current personal combined income tax rates for top marginal tax rate in 2025 are outlined below:

Increasing Basic Personal Income Tax Credits

In December 2024, the Government of Saskatchewan introduced the Saskatchewan Affordability Act to help address rising living costs. As part of the 2025–26 Budget, the Act will implement 13 measures aimed at reducing the tax burden on residents and businesses.

Key changes include annual increases of $500 over the next four tax years (2025 to 2028) to the basic personal exemption, spousal and equivalent-to-spouse exemptions, dependent child exemption, and senior supplementary amounts.

These enhancements will result in significant tax savings—for example, a family of four with an income of $100,000 will save over $3,400, while two seniors earning a combined $75,000 will save more than $3,100 over the same period. Once fully implemented, more than 54,000 individuals will no longer pay provincial income tax.

Increasing Disability and Caregiver Tax Credits

To further support those facing disability-related expenses, the Disability Tax Credit, the Disability Tax Credit Supplement for persons under 18, the Caregiver Tax Credit, and the Infirm Dependent Tax Credit will be increased by 25 percent in the 2025 taxation year.

Increasing the Low-Income Tax Credit

To provide further relief for Saskatchewan residents with low and modest incomes, the Saskatchewan Low-Income Tax Credit will be increased by 5 percent annually over the next four years. These increases will be in addition to the expected annual indexation increases of 2 percent in future years.

Increasing the Graduate Retention Program Tax Credit

To encourage more young people to live and work in Saskatchewan, the Graduate Retention Program’s Tax Credit will be raised by 20 percent for new postsecondary graduates who complete their studies on or after October 1, 2024.

Enhancing the Active Families Benefit

To better support Saskatchewan’s youth, the Active Families Benefit will be enhanced starting January 1, 2025. The refundable tax credit will double from $150 to $300 per child, and from $200 to $400 for children with disabilities. The income threshold for eligible families will also increase from $60,000 to $120,000, expanding access to the benefit for more households.

Introduction of the Fertility Treatment Tax Credit

To make fertility treatments more affordable, a new Fertility Treatment Tax Credit has been introduced, retroactive to January 1, 2025. The program offers a 50 percent refundable tax credit for one lifetime fertility treatment expense claim per tax filer for eligible treatments and expenses incurred in Saskatchewan. The maximum amount of eligible expenses that can be claimed is $20,000, which would result in a refund of up to $10,000 per eligible claimant.

Adjusting the Education property tax mill rates

To account for rising property assessment values, the 2025–26 Budget includes adjustments to education property tax mill rates across all property classes, effective January 1, 2025:

- Agricultural: reduced from 1.42 to 1.07;

- Residential: reduced from 4.54 to 4.27;

- Commercial/Industrial: reduced from 6.86 to 6.37;

- Resource: reduced from 9.88 to 7.49.

Home Renovation Tax Credit made permanent

Effective October 1, 2024, the Home Renovation Tax Credit is being reintroduced on a permanent basis. Homeowners can claim a non-refundable tax credit on up to $4,000 in eligible renovation expenses annually for their primary residence, providing a maximum benefit of $420 per year. Seniors are eligible for an additional $1,000 in qualifying expenses, increasing their maximum annual benefit to $525.

Increasing the First-Time Homebuyers’ Tax Credit

The 2025-26 Budget introduces an increase to the Saskatchewan First-Time Homebuyers’ Tax Credit from $10,000 to $15,000 for eligible home purchases, effective October 1, 2024. This increase raises the maximum benefit for an individual from $1,050 to $1,575. When combined with the federal tax credit, Saskatchewan first-time homebuyers will be eligible for a total income tax reduction of $3,075.

Corporate Income Tax Measures

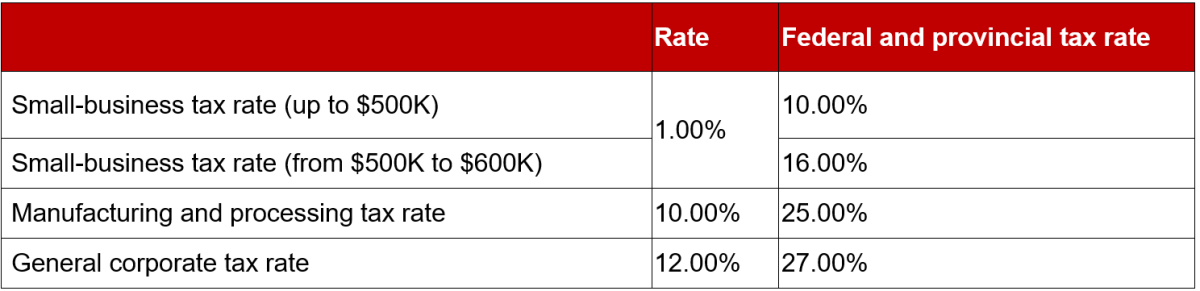

There are no proposed changes to corporate income tax rates or the $600,000 small-business limit for 2025. The corporate income tax rates for Saskatchewan in 2025 are as follows:

The 2025-26 Budget confirms that the Small Business Tax Rate will remain at the current rate of 1 percent instead of returning to 2 per cent as originally intended.

Introducing the Small and Medium Enterprise Investment Tax Credit

Starting July 1, 2025, the new Small and Medium Enterprise Investment Tax Credit will provide a non-refundable tax credit equal to 45% of the equity investment made by eligible individuals or corporations in qualifying small and medium-sized enterprises (SMEs).

The program will have an annual cap of $7 million in total tax credits, allocated on a first-come, first-served basis. To qualify, corporations must invest a minimum of $50,000 and individuals at least $25,000, with all investments subject to a minimum three-year holding period. Investors can earn up to $225,000 in tax credits per annual investment, and claim a maximum of $140,000 per eligible investment per year. Unused credits may be carried forward for up to seven years.

The program is intended to encourage private investment in local businesses, with further details to be released in the spring

Adjusting the Saskatchewan Commercial Innovation Incentive

The 2025–26 Budget extends the application deadline for the Saskatchewan Commercial Innovation Incentive (SCII) to June 30, 2027. This “patent box” incentive, introduced in 2017–18, offers eligible corporations a reduced provincial corporate income tax rate of 6% for 10 years on income from qualifying intellectual property commercialized in Saskatchewan. The benefit can be extended to 15 years if at least 50% of the related R&D was conducted in the province.

The program covers patents, plant breeders’ rights, trade secrets, and copyrights for computer programs and algorithms. To improve uptake, the Budget also reduces the scientific/technology test threshold and eliminates the economic benefits to Saskatchewan test.

Introducing the Low Productivity and Reactivation Oil Well Program

The 2025–26 Budget introduces the Low Productivity and Reactivation Oil Well Program, offering a Crown royalty and freehold production tax volumetric drilling incentive for low-producing, suspended, or inactive horizontal wells.

Under the program, eligible wells can receive a volumetric incentive of 3,000 cubic metres (m³) of production per newly drilled horizontal section, up to a maximum of 6,000 m³ per well. Each new section must be at least 500 metres in length.

The program applies to eligible wells drilled between April 1, 2025, and March 31, 2029.

Extending the Oil Infrastructure Investment Program

The 2025–26 Budget extends the Oil Infrastructure Investment Program’s application period until March 31, 2029, and extends the deadline for claiming royalty credits on completed projects from 2035 to 2040.

To qualify, projects must involve a minimum investment of $10 million in approved capital expenditure.

First introduced in the 2019–20 Budget, the program offers transferable Crown royalty and freehold production tax credits at a rate of 20% of eligible project costs for projects that significantly increase provincial pipeline capacity. Eligible projects include new or expanded pipelines for oil, refined petroleum products, natural gas liquids, and carbon dioxide, as well as related infrastructure investments.

Indirect Tax Measures

PST Rebate for New Home Construction

Originally introduced in the 2020–21 Budget and expanded in 2023, the Provincial Sales Tax (PST) Rebate for New Home Construction is now being made permanent. The program provides a rebate of up to 42% of the PST paid on the purchase of a new, previously unoccupied home, with a total price under $550,000 (before taxes and excluding the value of land, furniture, furnishings, and appliances). The rebate is gradually phased out for homes priced between $450,000 and $550,000.

Taxation of electric vehicles

To better reflect road maintenance costs and ensure electric vehicle (EV) owners contribute more comparably to traditional vehicle owners, the annual Road Use Charge for passenger EVs will increase from $150 to $300 starting in the 2025-26 Budget, effective June 1, 2025.

Applying the PST on vapour products

To ensure tax fairness and discourage the appeal of vapour products to youth and non-smokers, the Provincial Sales Tax (PST) base will be expanded to include the sale of all vapour liquids, products, and devices, effective June 1, 2025.

Eliminating the Lloydminster vapour products tax exemption

Starting in 2025, Alberta will join the federal Coordinated Vaping Products Taxation Agreement, which introduces a provincial duty on vapor products. As a result, the vapor products tax exemption in Lloydminster will be removed, effective June 1, 2025.