Navigating the Impact of the Proposed US Tariffs on Canadian Businesses

Overview

The ongoing trade tensions escalating between the US and Canada are creating an atmosphere of economic uncertainty for Canadian businesses. Canada’s largest trading partner is the US, amounting for approximately 70% of its total exports. Canadian businesses most heavily reliant on cross-border trades with the US are facing the greatest uncertainty.

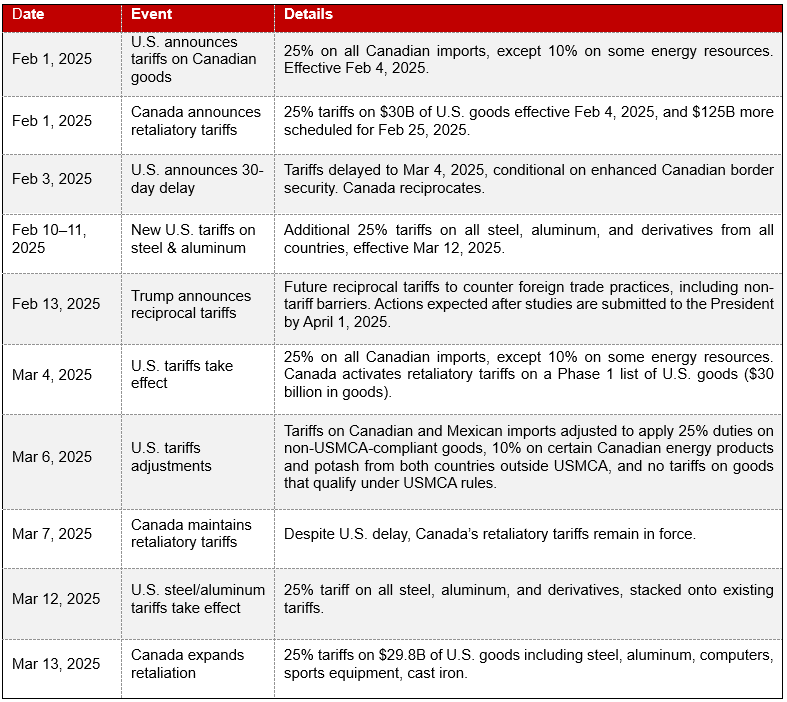

On February 1st,2025, US President Donald Trump signed an executive order imposing a 25% tariff on all Canadian imports (except for some energy resources that would be subject to a 10% tariff instead) effective February 4, 2025.

In response to U.S. President Donald Trump’s announcement, Prime Minister Justin Trudeau declared retaliatory measures. These measures included the imposition of 25% tariffs on $30 billion worth of US imports initially set to take effect on February 4, 2025 with additional 25% tariffs on $125 billion worth of US imported goods scheduled for February 25, 2025.

A few days following the signing of the US tariffs’ execution order, President Trump announced a 30-day delay of the enactment of the proposed tariffs, which were scheduled to take effect on March 4th.This delaywas agreed because, according to President Trump, Government of Canada has taken immediate steps designed to alleviate the illegal migration and illicit drug crisis through cooperative actions.

On February 10th and 11th, President Trump signed two executive orders imposing a new separate 25% tariff on imports of steel and aluminum products from all countries starting March 12th (these new tariffs would be stacked onto those previously announced). Further, President Trump announced on February 13th that he would be imposing reciprocal (and additional) tariffs in response to the perceived discriminatory trade practices/taxes from other countries (e.g., Canada’s digital service tax, Canada’s goods and services tax (“GST”, etc.)).

On March 4, 2025, the U.S. tariffs officially took effect, applying a 25% tariff on all Canadian imports, with a reduced 10% rate for certain energy resources. On the same day, Canada activated its Phase 1 retaliatory tariffs on $30 billion worth of U.S. goods.

However, on March 6, 2025, President Trump signed executive orders to adjust the tariffs imposed on imports from Canada and Mexico as follow:

- Duties imposed to address the flow of illicit drugs across our borders are now:

- 25% tariffs on goods that do not satisfy U.S.-Mexico-Canada Agreement (USMCA) rules of origin.

- A lower 10% tariff on those energy products imported from Canada that fall outside the USMCA preference.

- A lower 10% tariff on any potash imported from Canada and Mexico that falls outside the USMCA preference.

- No tariffs on those goods from Canada and Mexico that claim and qualify for USMCA preference.

Despite this adjustment, Canada maintained its retaliatory tariffs, as confirmed on March 7, 2025.

On March 12, 2025, the U.S. steel and aluminum tariffs took effect, imposing a 25% tariff on all steel, aluminum, and derivative products, applied on top of any existing tariffs. In response, on March 13, 2025, Canada expanded its retaliation, imposing 25% tariffs on an additional $29.8 billion worth of U.S. goods, including steel, aluminum, computers, sports equipment, and cast iron products.

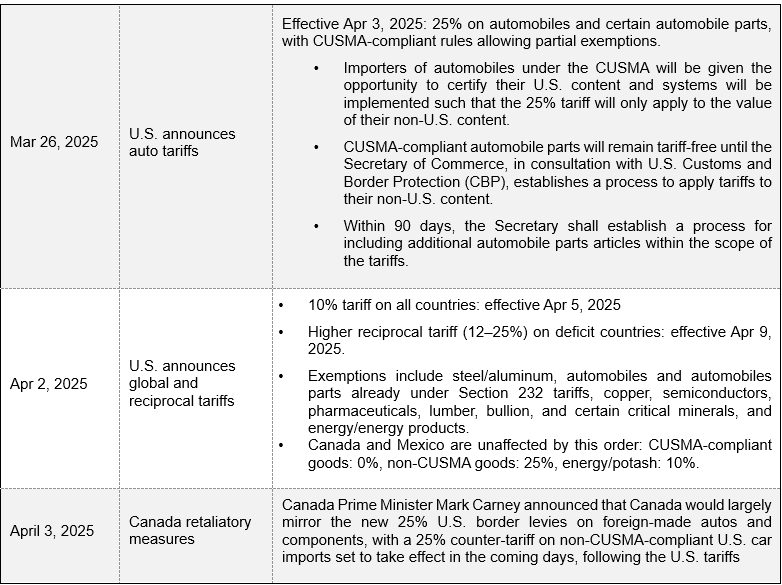

On March 26, 2025, the U.S. announced a new round of tariffs targeting the automobile sector, effective April 3, 2025. These tariffs impose a 25% duty on automobiles and certain automobile parts that will only apply to the non-U.S. content. That said, CUSMA-compliant automobile parts will remain tariff-free until the Secretary of Commerce establishes a process for applying tariffs to their non-U.S. content.

Finally, on April 2, 2025, the U.S. announced a sweeping set of global and reciprocal tariffs. A 10% tariff on imports from all countries will take effect April 5, 2025, followed by higher “reciprocal” tariffs (ranging from 12% to 25%) on imports from countries with significant trade surpluses with the U.S., effective April 9, 2025. Several categories of goods will be exempt from this regime, including steel, aluminum, automobiles already covered by Section 232 tariffs, copper, semiconductors, pharmaceuticals, lumber, bullion, and critical energy or mineral imports that are unavailable domestically. Canada and Mexico will remain unaffected under this new order.

This is not the first time that Canadian businesses have faced uncertainty amid US imposed tariffs. As businesses face these looming and everchanging tariffs, they should look to review/adjust their operational strategies (e.g., supply chains, sourcing, distribution and manufacturing locations) to determine if the financial impact of these tariffs can be lowered and or mitigated. Businesses should also review/adjust their tax strategies (e.g., customs, sales tax, transfer pricing). Andersen can assist your business in reviewing these strategies.

Tariffs 101 – Impact of Canadian Businesses

A tariff is a tax levied by a nation’s government on the import of goods from another country and is generally paid by the person or company that imported them (e.g., importer of record). Tariffs are collected by the government that imposes them; they are not paid by one government to another.

The customs value, also known as the value for duty (“VFD”), is the basis for calculating duties and taxes applicable and it is declared by the importer. There are six methods for calculating the VFD, and each of these methods have a specific calculation that importers must follow to determine the correct VFD. It should be noted that the Canada Border Services Agency (“CBSA”) has stated that importers should always use the “transaction value method” to determine the VFD of an imported good unless it is impossible to do so. Although certain trade incentives, such as duty drawbacks and reliefs have been applicable in the past, the current tariffs to be imposed under President Trump recent executive orders will be ineligible for duty drawback. That is, importers cannot obtain refunds for these specific tariffs, even if the goods are subsequently exported or destroyed. [1]In Canada, the CBSA is responsible for administering and collecting duties and taxes on imported goods, including tariffs. The US equivalent is the US Customs and Border Protection agency (“USCBP”).

As a result of the impending tariffs, both Canadian importers and exporters will be impacted:

- Importers: Canadian-imposed tariffs (including the proposed 25% US retaliatory tariffs) can drive up the cost of making the product. Canadian companies that import goods or raw materials from the US would likely face higher costs for their manufacturing inputs, affecting their overall production expenses. This increase in costs can lead to higher prices for finished goods, further eroding competitiveness. Companies might also experience supply chain disruptions if they are unable to source materials from the US at affordable rates. To compensate for this, businesses would either have to charge more for the finished product or accept a lower profit.

For example, manufacturing businesses which are heavily reliant on US imports for raw materials, are particularly vulnerable to these tariff increases.

- Exporters: Foreign-imposed tariffs (including the proposed 25% US tariffs on all Canadian imports) are a trade barrier that make it harder to compete in international markets by raising prices for goods and relating services. That is, it raises the cost of Canadian products entering the US market, making them less competitive compared to local or foreign alternatives. This would likely lead to decreased demand, lower export volumes, and potential revenue losses for Canadian businesses.

For example, industries such as automotive, steel, and agricultural products, which are heavily reliant on exports to the US, are particularly vulnerable to these tariff increases.

It is important to note, that subject to exception, all goods imported into Canada are also subject to the 5% goods and services tax (“GST”) (and the provincial part of the harmonized sales tax (“HST”) or the Québec Sales Tax (“QST”)/provincial sales tax (“PST”) – for non-commercial imports). The CBSA collects these at importation along with any applicable duties and excise taxes.

Although the Canadian federal government is proposing certain measures to ease the effects of these tariffs, these measures may not be applicable to all businesses and likely not long-term solutions. There are however mitigating strategies that businesses can employ that can help them reduce the financial impact of these blanket tariffs.

How can businesses reduce financial disruptions caused by these tariffs?

On the shorter term, businesses operating in industries that are less sensitive to price stickiness can attempt to pass on the costs of the tariffs (in whole or in part) to their customers, while others may consider diversifying their purchases and sourcing materials from non-US suppliers[2]. For those businesses that are unable to fully pass on the costs of tariffs and or will continue to depend heavily on the US market for their business survival and success, there are some longer-term strategies that can be considered:

- Shifting activities to the US: Canadian businesses can review and adjust their current operating model, especially in cases where they own/control their entire business cycle (e.g., manufacturing, distribution), with the objective of reducing the overall financial impact of the tariffs within the group:

- Shifting distribution activities: Canadian businesses that are currently selling directly to third parties in the US market could consider shifting their distribution/selling activities to a US related party/subsidiary. In addition, businesses can also consider acquisitions in the US to maintain access to their customers. Through transfer pricing strategies, as further discussed below (e.g., potential reduction in the intercompany transfer price of good), businesses can reduce the financial impact of these tariffs.

- Shifting Manufacturing capabilities: Canadian businesses could shift manufacturing activities (all or in part, including the transfer of any related intangible property/assets) to the US. Businesses. It could also consider shifting its manufacturing activities to non-US jurisdictions with lower tariffs. However, given the Trump Administration’s recent tariff threats on other countries, this may become a less attractive option.

- Supply Chain/Inventory Management: Canadian manufacturers could opt to store goods in Canadian warehouses until such goods would then be sold on the US market (and that point transported) to avoid paying tariffs on unsold/inventoried products in the US (or vice-versa). Although this may not remove the financial impact of tariffs it could reduce/delay it.

For those Canadian businesses that do not yet have a physical presence in the US and are considering either the creation of a US subsidiary/branch and or the acquisition of a US company, there are various tax considerations that should be factored into their decision-making process. These include but are not limited to, US/Canadian corporate tax, transfer pricing, withholding tax, indirect tax and customs implications.

- Optimizing transfer pricing strategies: Canadian businesses currently transacting with related parties in the US, could review/optimize their current transfer pricing model with the objective of reducing the overall financial impact of the tariffs within the group.

- Adjusting transfer pricing returns: Adjusting returns within the arm’s length range could have a direct impact on the transfer price of a good on which a tariff may be applied. For example, if the profitability of a US distribution were to be increased, this could lower the VFD of goods and the resulting tariff cost (all dependent on the customs method employed).

- Unbundling transfer prices: Businesses could look to unbundle their transfer prices, where applicable, to carve out potential non-tariff components (e.g., intangible property royalties, management/service fees), to effectively lower the VFD of goods being imported and subject to the tariffs. Business however need to ensure that any unbundling of the transfer prices respects the customs valuation method that is being employed.

- Restructuring the group’s business activities: Restructuring a multinational group’s operating model, including the reallocation or shifting of functions, assets, or risks from one entity of the group to another (e.g., shifting manufacturing capabilities, setting up a US distribution entity, transferring/selling intangible property) could lead to shifts in profit allocation among these entities/jurisdictions that could have a direct on the VFD of goods on which the tariffs apply.

As a result of the Trump Administrations’ 25% tariff on imports of steel and aluminum products from all countries, including Canada, multinational groups that rely heavily on the US market may consider the shifting of activities on a more global scale.

- Reviewing contracts and Incoterms: Businesses should review their intercompany and or third-party arrangements to determine tariff responsibilities and ensure clarity on duty liabilities. In addition, adjusting Incoterms and/or renegotiating contracts to align with new tariff risks may be beneficial.

Businesses looking to make changes to their operational and or transfer pricing model should ensure that they consider any corresponding business, tax and customs implications of such changes. This includes the termination of existing agreements, sale/transfer of tangible and or intangible assets, exit payments, indirect taxes[3], customs VFD, etc. In addition, proper transfer pricing documentation is essential to ensure that any changes (e.g., business restructurings) comply with Canadian and US transfer pricing rules.

Transfer prices vs. VFD

For multinational groups, transfer pricing and VFD (on which tariffs apply) are intertwined. From a transfer pricing perspective, the determination of the prices at which services, tangible property, and intangible property are traded across international borders between related parties is made under the Income Tax Act (“ITA”)[4]. From a customs perspective, the determination of the VFD of imported goods is made under the Customs Act. While both the Canada Revenue Agency (“CRA”) and the CBSA administer aspects of Canadian taxation, the two have competing tasks when determining / assessing the price of imported tangible goods.

- The CRA is looking to fairly apply rules concerning income taxation to maximize income tax payable by a company.

- The CBSA focuses on ensuring that the VFD of goods imported accurately reflects all dutiable cost elements and looks to ensure the VFD is not depressed through transfer pricing and that duties paid are maximized.

As such, these concepts compete as higher import values generally result in lower taxable income (for Canadian businesses). Although the underlying principles for establishing inter-company selling prices are the same, this does not necessarily mean that a transfer price that is acceptable for income tax purposes will be suitable for customs purposes, and vice versa. Given that the CBSA is second only to CRA in revenue collection in Canada businesses can likely expect increased (and adverse) audit activity with respect to their transfer prices and VFD. Robust documentation in support of the transfer prices and VFD are crucial in navigating through these new tariffs and potentially mitigating any upcoming adverse audit risks.

Next Steps / Tariff Readiness

Businesses should continue to monitor the status of the ongoing trade negotiations as well as monitor key dates. Our tax practice can help businesses in evaluating various tariff’s related tax challenges and opportunities, including international corporate restructuring and planning, due diligence reviews, transfer pricing, customs, sales tax, CRA and CBSA audits, etc.

We encourage businesses to discuss potential tariff related questions, implications and or concerns with their Andersen tax advisor.

Andersen Canada Contacts

| Danny Guerin, CPA, LL.M.Fisc. Partner, Andersen Montreal |  | Nicolas Rondeau, CPA Indirect Tax Director, Andersen Montreal |

[1] Business should be aware that certain trade incentive programs, such as duty drawbacks and reliefs, may still be applicable to the import of certain goods from a Canadian perspective.

[2] The Canadian government has considered removing interprovincial trade barriers to strengthen Canada’s economy. It has committed to removing regulatory obstacles, standardizing industry certifications, and facilitating labor mobility to boost economic efficiency.

[3] As previously notes, subject to exception, all goods imported into Canada are also subject to the 5% GST (and the provincial part of the HST or the QST/PST – for non-commercial imports).

[4] Section 247 of Canada’s ITA.