Budget 2022-2023 – Québec Ministry of Finance

Prepared by Andersen in Canada, Montréal Partner Patrick Coutu, Tax Managers Divya Katyal and Catarina Marques with support from Inta Simonyan.

On March 22, 2022, the government of Québec released its 2022-2023 budget. Below is an overview of some of the major proposals:

1. COST OF LIVING LUMP SUM PAYMENT

Every Québec resident aged 18 years or older declaring a net income of $100,000 or less in their tax return for fiscal year 2021 will receive an automatic refundable tax credit of $500.

The receipt of this credit is automatic upon filing the 2021 tax return and the amount of the credit can be used to offset any tax payable.

This tax credit is reduced at a rate of 10% for every dollar of personal net income earned exceeding $100,000.

This measure is combined with the payment of the extraordinary cost of living allowance announced earlier this year.

2. QUÉBEC RESEARCH AND INNOVATION STRATEGY 2022-2027

Québec has renewed for another 5 years its tax incentives package for R&D and intellectual property development activities which includes the following measures:

- Businesses that engage in R&D activities in Québec can keep claiming R&D tax credits for up to 30% of R&D expenses for small and medium businesses and 14% for large corporations.

- Foreign researchers and experts engaging in R&D activities in Québec for a Québec company may continue to benefit from a tax holiday: a degressive deduction is applied to their taxable income of 100% for the first 2 years, 75% for the third year, 50% for the fourth year and 25% for the fifth and last year.

- A corporation commercializing intellectual property in Québec may, under certain circumstances, benefit from a 2% taxation rate on income derived from this intellectual property.

3. INVESTMENT AND INNOVATION TAX CREDIT (C3i)

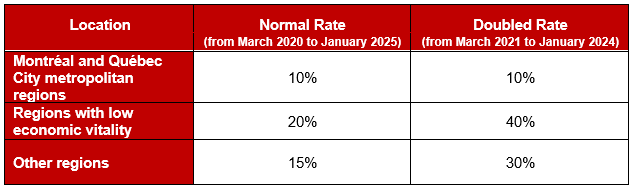

This credit for acquiring new technologies to digitize processes and upgrade equipment sees its doubled rates continuing until January 1, 2024.

Corporations operating a business and having an establishment in the province can deduct the following eligible property if it was acquired after March 10, 2020, and before January 1, 2025:

- Manufacturing and processing materials (class 43 or 53) valued at $12,500 or more per item;

- Computer equipment (class 50) valued at $5,000 or more per item; and

- Management software (class 12) valued at $5,000 or more per item.

Corporations may also deduct expenditures related to the above-mentioned items provided they exceed the applicable minimum thresholds.

The rate of the tax credit varies depending on the location of the investment as shown in the table below:

The tax credit is fully refundable for corporations with assets and gross revenue not exceeding $50 million and partially refundable for those with assets and gross revenue of less than $100 million.

This incentive is capped at $100 million of eligible investment expenditure over 5 years.

4. THE “ROULEZ VERT” (ELECTRIC VEHICLE INCENTIVE) PROGRAM

Rebates for electric vehicle purchases as well as purchases and installation of electric charging stations will continue to be funded until 2027.

The maximum rebates granted for electric vehicle acquisitions will be, as of April 1, 2022:

- $7,000 for new fully electric vehicles;

- $5,000 for new plug-in hybrid vehicles; and

- $3,500 for used fully electric vehicles.

The rebate amounts for future tax years will be announced at a later date.

5. TAX CREDITS FOR BIOFUELS AND PYROLYSIS OIL PRODUCTION

Québec’s existing tax assistance measures for biofuel and pyrolysis oil production will be expiring on March 31, 2023.

Thus, Québec will be introducing new biofuel and pyrolysis oil production tax credits which will be in effect from April 1, 2023 to March 31, 2033.

To benefit from these tax credits, production activities must take place in the province of Québec, the biofuel or pyrolysis oil must be sold and used in the province. Furthermore, the taxpayer will need to obtain a qualification certificate from the Minister of Energy and Natural Resources to obtain the tax credits.

Each of the new tax credits will be capped at a maximum amount of 300 million litres.

More information about the new tax credits is expected in the future.

6. CULTURAL SECTOR SUPPORT

Québec is allocating additional amounts to extend certain support programs for the entertainment and culture sectors to offset the effects of COVID-19.

7. TAX CREDIT FOR CULTURAL DONATION

The tax credit for first major cultural donation is now permanent.

An individual who makes a first cash donation of at least $5,000 and up to $25,000 to a cultural organization over the course of the year is eligible for a non-refundable tax credit equal to 25% of the amount donated.

8. TAX CREDITS FOR RESIDENTIAL WASTEWATER TREATMENT

The tax credit for the upgrading of residential wastewater treatment systems is extended for another five years. It provides homeowners who upgrade their systems with a maximum assistance of $5,500.

9. REVENU QUÉBEC’S “VISION” PROJECT

Revenu Québec is simplifying its tax administration model through an expanded digital offering of services. This investment aims to reduce tax administration burdens on taxpayers.

10. HOTEL ACCOMMODATION TAX REFUND PROGRAM

Québec will be providing amounts to renew the accommodation tax refund program through 2022.

11. SUBSIDY FOR TOURISM INDUSTRY

The tourism industry Program Supporting the Development of Tourist Attractions (PADAT) received additional amounts in order to allow businesses to invest in the industry and increase the number of accommodation units available.

12. SUPPORTING THE DEVELOPMENT OF FLIGHT CONNECTIONS

An amount is allocated to support the development of new international direct flight connections to Québec airports.

13. CHANGES IN INTERRUPTION OF PRESCRIPTION PERIOD RULES

Québec’s Tax Administration Act states that the recovery of amounts owed under a fiscal law become statute-barred after 10 years. However, in certain cases, this 10-year period may be suspended or interrupted.

Among other situations, the prescription is interrupted when the Minister of Revenue applies a tax refund to the payment of the taxpayer’s fiscal debt. Each time such an event takes place, the prescription period is interrupted and begins anew.

Québec has chosen to eliminate the above-described event as a cause for interrupting the prescription period.

This measure will take effect on a date determined by the government of Québec.