Overview

On March 18, 2026, Quebec’s Minister of Finance, Eric Girard, tabled the province’s 2026–2027 Budget, titled “A responsible budget with targeted measures for Quebecers”.

The Budget is presented amidst geopolitical uncertainty, trade tensions, and continued increasing cost-of-living pressures. It emphasizes fiscal discipline, targeted support, and economic transformation, while maintaining the government’s objective of returning to a balanced Budget by 2029-2030.

From a tax policy perspective, the Budget introduces limited broad-based changes, instead focusing on targeted adjustments to selected existing tax credits and administrative measures.

This comprehensive summary highlights some of the key changes that will influence the Quebec tax environment in the coming years.

Personal Income Tax Measures

There are no proposed changes to personal income tax rates for 2026.

The income tax rates for the 2026 taxation year, based on taxable income, are as follows:

| Taxable income | Rate |

| $54,345 or less | 14.00% |

| Over $54,345 up to $108,680 | 19.00% |

| Over $108,680 up to $132,245 | 24.00% |

| Over $132,245 | 25.75% |

The current combined personal income tax rates for the top marginal bracket in 2026 are detailed below for each type of income:

| Taxable income exceeding $258,482 | Rate |

| Interest/regular income | 53.31% |

| Capital gains | 26.65% |

| Eligible dividends | 40.11% |

| Non eligible dividends | 48.70% |

Automated Income Tax Filing for Certain Low-Income Individuals

Revenu Quebec has undertaken various initiatives in recent years to simplify the tax filing process for vulnerable low-income individuals. Notably, a pilot project allowed selected taxpayers to provide basic information so that Revenu Quebec could prepare and file their returns on their behalf. Despite these efforts, barriers to filing remain for certain taxpayers.

Accordingly, starting with the 2026 taxation year, Revenu Quebec will implement an automated income tax filing process for eligible low-income individuals. Legislative amendments will be introduced to allow Revenu Quebec to file income tax returns on behalf of such individuals.

Eligibility criteria, focusing on individuals with a simple and stable tax profile, will be established by spring of 2027 and will apply starting with the 2026 taxation year.

Changes to the Voluntary Retirement Savings Plan (“VRSP”)

The budget is providing clarifications with respect to the VRSP, establishing a minimum contribution rate of 2% of salary, simplifying the administration of contributions and introducing new investment options with employer contributions

Corporate Income Tax Measures

There are no proposed changes to the general (and M&P) corporate income tax rates or the $500,000 small-business limit for 2026.

The corporate income tax rates for taxpayers having a taxable presence in Quebec for 2026 remain as follows:

| Provincial tax rate | Federal and provincial combined tax rate[1] | |

| Small-business tax rate[2] [3] | 3.20% | 12.20% |

| General and M&P corporate tax rate | 11.50% | 26.50% |

Amendments to the Refundable Tax Credit to Support Print Media

Introduced in 2019, the refundable tax credit to support print media was intended to address the challenges faced by the print journalism industry resulting from changes in media consumption habits. This measure aimed to support activities related to the production and dissemination of quality public-interest information in Quebec.

In the 2026-2027 Budget, the government announced enhancements to such measure. The following represent the proposed amendments to the legislation:

- the expansion of eligible organizations to include news agencies and broadcasters of news programs on radio and television.

- the increase in the annual eligible wage cap from $75,000 to $85,000 per eligible employee, allowing for a maximum refundable tax credit of $29,750 per employee; and

- the refocusing of eligible activities by excluding information technology activities for the purposes of the employee certificate.

The changes will apply to a taxation year ending after the day of the Budget speech.

Extension and Phase-Out of the Refundable Tax Credit for the Digital Transformation of Print Media

Prior to the 2026-2027 Budget, a qualified corporation carrying out eligible digital transformation activities for an eligible print media outlet could benefit from a refundable tax credit at a rate of 35% applicable to all qualified expenditures. The eligibility period, which was scheduled to end on December 31, 2025, is now set to be extended to December 31, 2028, while introducing a gradual phasing-out period for the credit.

Amendments will be made so that the tax credit rate, which is currently 35%, will be reduced to 20% in 2027 and 10% in 2028.

Amendments to the Refundable Tax Credit for Quebec Film or Television Productions

The 2026-2027 Budget introduces targeted adjustments to refundable tax credit for Quebec film or television productions. In particular:

- Financial assistance from the Indigenous Screen Office will be excluded from assistance amounts for the purposes of the refundable tax credit, such that it will no longer reduce eligible expenditures; and

- Eligibility criteria will be revised for certain classes of productions, such that audiovisual magazine programs and documentaries will no longer be required to meet minimum thresholds relating to the duration of content or number of episodes to qualify.

These amendments will apply to applications filed with SODEC after the date of the Budget speech.

Consequential amendments will also be made to the tax credit for film dubbing and the tax credit for film production services to ensure consistency in the treatment of eligible production classes.

Adjustments to the Tax Credit for the Development of E-business Integrating Artificial Intelligence Functionalities (TCEBAI)

Introduced in the 2025–2026 Budget, the Tax Credit for the Development of E-Business Integrating Artificial Intelligence (TCEBAI) replaced the former Tax Credit for the Development of E-Business (TCEB). This new regime is intended to promote higher value-added IT activities by focusing tax support on artificial intelligence-driven solutions.

The 2026-2027 Budget introduces amendments intended to enhance the usability and predictability of the TCEBAI. These amendments include:

- the addition of specialized AI consulting services to the list of eligible activities.

- the recognition of preparatory work carried out within 12 months preceding the start of an eligible mandate or project.

- the relaxation of employee certificate criteria to account for activities necessary for the effective integration of AI into business solutions.

Additionally, the amendments will clarify the application of the reduced credit rates for corporations that carry out intercompany outsourcing. More specifically, the 50% gross revenue test will explicitly include revenues from non-arm’s length transactions, including support and maintenance revenue.

Finally, as part of the transition from the TCEB to the TCEBAI, prior rules effectively restricted the use of certain non-refundable tax credit balances generated under the former regime. To avoid unduly disadvantaging corporations in this situation, the Budget provides that legislation will be amended, for non-refundable tax credit balances generated before January 1st, 2026, to remove the condition whereby carry-overs could only be applied against a taxation year in which the corporation obtains the refundable tax credit.

The above changes apply to balances arising in taxation years beginning after December 31, 2025.

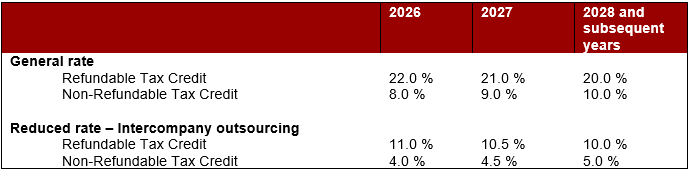

Applicable TCEBAI tax credit rates

Other tax measures

Harmonization with Federal Immediate Expensing for Greenhouse Buildings

Following the federal government’s announcement introducing an immediate expensing measure for greenhouse buildings[4], Quebec has indicated that it will harmonize[5] its tax legislation and regulations accordingly.

Adjustments to Certain Disclosure Mechanisms

The Budget proposes amendments to simplify the filing of mandatory disclosure information returns.

These amendments are intended to streamline filing requirements for taxpayers subject to mandatory disclosure rules and facilitate compliance with existing reporting obligations.

More specifically, the adjustments include:

- removing the reference to the method of transmission of information returns.

- removing the reference to the proof of receipt of information returns.

- removing the compliance presumption regarding the 120-day period granted to tax authorities to request additional information concerning an information return.

These changes will apply as of the date of the Budget speech.

For more information, visit https://www.finances.gouv.qc.ca/Budget_and_update/Budget/index.asp

[1] Federal corporate income tax rates on qualifying zero-emission technology manufacturing profits are temporarily reduced by 50%, lowering the general rate to 7.5% (from 15%) and the CCPC rate to 4.5% (from 9%), for taxation years from 2022 through 2031. These reduced rates will then be gradually phased out for taxation years beginning in 2032 through 2034.

[2] Applies to the first $500,000 of active taxable income of Canadian-Controlled Private Corporations (CCPCs).

[3] The Quebec small business deduction is available to companies whose employees have worked at least 5,500 paid hours during the taxation year. The deduction is progressively reduced for businesses having between 5,000 and 5,500 paid hours and is eliminated if paid hours fall below 5,000. However, some corporations in the primary or manufacturing sectors may not subject to this requirement.

[4] GOVERNMENT OF CANADA, Prime Minister Carney announces new measures to make groceries and other essentials more affordable for Canadians, [Online], January 26, 2026,

[5] For buildings acquired on or after November 4, 2025, and that become available for use before 2030.

Contact Our Team Of Experts

This article was prepared by the individuals listed below. For further information on the above, we invite you to please reach out to Danny Guérin of Andersen Inc.

| Danny Guérin, CPA, LL.M.Fisc. Partner |  | Seihavy Ing, LL.B., M.Fisc. Manager |  | Irvin Jay Sarenas, CPA, Senior Manager |