Carbon tax: a contentious tax

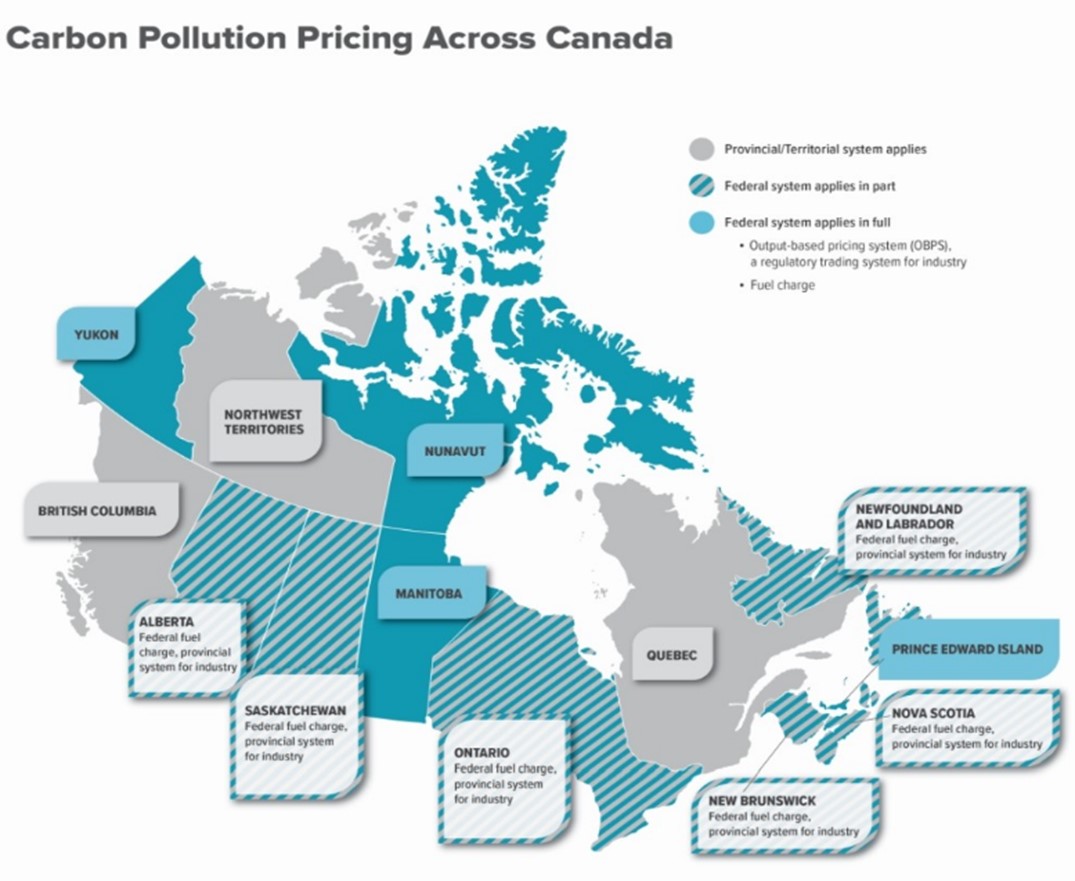

The Greenhouse Gas Pollution Pricing Act (“GGPPA”), which came into force on June 21, 2018, mandates that all provinces and territories are to implement a carbon pricing system that meet federal benchmarking criteria or be subject to the federal pricing system.

Several provinces, including Alberta, Ontario, and Saskatchewan, have been strongly opposed to a federal carbon tax, claiming that natural resources fall under provincial jurisdiction according to the Canadian Constitution.

In a six-to-three decision issued on March 25, 2021, the Supreme Court of Canada (“Court”) confirmed the constitutionality of the GGPPA, allowing Ottawa to move forward with its plan to implement carbon pricing across all provinces and territories. The Court ruled that setting minimum pricing standards is justified due to the national importance of climate change and the need for a coordinated response to this issue that goes beyond provincial boundaries.

Overview of relevant laws and regulations

The GGPPA sets minimum standards for provinces and territories of Canada. Provinces and territories can design their own carbon pricing systems tailored to local conditions, as long as they meet federal benchmarks. These systems can include fuel charge, carbon tax, cap-and-trade programs, or a combination thereof.

Source: Government of Canada, 2024-09-18

The GGPPA includes two pricing systems:

- Part 1: The fuel charge. Targets businesses in the fuel supply chain.

- Part 2: Output-based pricing system (“OBPS”). Targets large industrial emitters which are referred to as “covered facility” (i.e. a facility or property in Manitoba, Prince Edward Island, Yukon or Nunavut and either (a) meets the criteria set out in the regulations for that province or territory; or (b) is designated by the government as a covered facility).

The federally regulated provinces and territories are referred to as “listed provinces” in the present paper.

The fuel charge

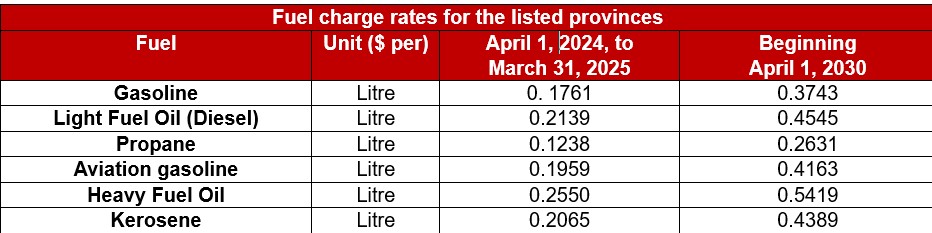

The fuel charge is levied on various carbon-based fuels, including but not limited to, gasoline, diesel, natural gas, propane, and aviation fuel, as listed in Schedule 2 of the GGPPA (“regulated fuel”)[1]. The rate for each regulated fuel reflects a carbon pollution price, which will increase from CA$80 a ton to CA$95 a ton on April 1, 2025 – and up to CA$170 in 2030. The rates are also based on Global Warming Potential and emission factors used by Environment and Climate Change Canada to report Canada’s emissions to the United Nations Framework Convention on Climate Change. Below is a table showing the projected rates for common regulated fuels from April 1, 2024, to April 1, 2030:

Andersen preliminary observations

It is important to note that the GGPPA is a complex law with numerous exceptions that grants the federal government with broad regulatory authority to introduce additional factors, particularly in registration requirements, exemption certificates, and the application of the fuel charge. While this discretion allows the government to adapt the fuel charge mechanism in response to evolving environmental policies, changes in fuel usage, evolving technology and practices or other logistical considerations, it also makes the GGPPA a work in progress. This discretion can create regulatory uncertainty and increase the system’s complexity. Therefore, it is essential for businesses to consult with a tax professional to ensure that their operations comply with these specific regulations.

The purpose of this paper is to provide general information; however, given the complexity of the GGPPA and the numerous exceptions it contains, each situation should be assessed individually for an accurate and tailored evaluation.

Registration

- Distributor

- Importer

- Emitter

- User

- User of Combustible Waste

- Air Carrier and Specified Air Carrier

- Marine Carrier and Specified Marine Carrier

- Rail Carrier and Specified Rail Carrier

- Road Carrier

A person may be required to register under multiple types depending on their activities and may hold multiple registrations for different types of regulated fuel. However, only one registration for a specific regulated fuel is required across all listed provinces.

Registration is made using the form L400 Fuel Charge Registration and the associated schedules:

- L400-1 Fuel Charge Registration Schedule: Details the registration type by regulated fuel type. Required for all types of registration except road carriers.

- L400-2 Fuel Charge Registration Schedule – Road Carrier: Details the regulated fuel types by listed province. Required only for road carriers.

- L400-3 Non-Resident – Records kept outside Canada: Required only for non-residents that keep records outside Canada.

Refer to Appendix 1 for an overview of the registration requirements by type of activity.

Paying (remitting) the fuel charge

When applicable, the fuel charge is calculated by multiplying the total quantity of regulated fuel on which the charge is applied with the fuel charge rate of the specific period and province when the charge becomes payable. Thus, a separate calculation is needed for each federally regulated province and each registration type held by the registrant. For persons registered under a “carrier” type of registration (e.g. Air, Marine, Rail and Road Carriers – specified and non-specified), the charge is calculated on the net fuel quantity of regulated fuel used, delivered, or transferred in the listed province.

The carbon pollution price is adjusted on April 1st of each year. The GGPPA therefore provides a mechanism called “adjustment days”, which triggers the application of the fuel charge on April 1st of each year, and targets non-registered persons as well. The amount payable is the difference between the new fuel charge rate that comes into effect on April 1 and the previous lower rate from before the increase calculated on the regulated fuel that the person holds in a listed province. Certain exemptions apply, such as holding the fuel as a registered distributor or specified carrier; or the amount being less than $1,000.

A registered person must file Form B400, Fuel Charge Return – Registrant, and associated schedules monthly, and pay any fuel charge payable by the end of the month after the charge was payable. There are however a few exceptions where a person can file quarterly. When a non-registrant is required to self-assess the fuel charge, they must file Form B401 Fuel Charge Return for Non-registrants which typically applies when they import, bring into, produce, or burn combustible waste in a listed province.

Refer to Appendix 2 for an overview of the circumstances that trigger the fuel charge.

Rebates

Under the GGPPA, several scenarios allow for rebates on the fuel charge.

- A registered emitter, user, importer, or carrier who removes fuel from a listed province can receive a rebate if the fuel was previously subject to the charge when it was brought into or removed from a covered facility, or if the facility ceased to be covered.

- Registered emitters bringing fuel to a covered facility in a listed province are also eligible for a rebate on fuel that was previously charged when brought into the province, removed from a covered facility, or held in a facility that ceased to be covered.

- Registered users can claim a rebate for fuel used in non-covered activities at non-covered facilities in a listed province, provided the fuel was previously subject to the charge upon importation or entry into the province. Non-covered activities include industrial processes where fuel is used as a raw material and not burned or flared.

- If a person overpaid the fuel charge, whether due to a mistake or another reason, they could be entitled to a rebate. Such rebate only applies to fuel charge self-assessed under the GGPPA and does not include any fuel charge paid by being buried in the price of a certain fuel.

The GGPPA also allows for flexibility through regulations to prescribe specific circumstances that may trigger a rebate of the fuel charge.

Anti-avoidance

Administration and enforcement

The GGPPA establishes a robust framework to ensure compliance with the fuel charge. This includes provisions for reassessments, penalties for late payments, and interest on overdue amounts. The Canada Revenue Agency (“CRA”) has the authority to issue notices of assessment and conduct audits to verify compliance. There are also rules governing when returns must be filed and how records should be maintained for audit purposes. If a person disagrees with an assessment or decision, they may file an objection. If they remain unsatisfied, they can appeal to the Tax Court of Canada. Additionally, the GGPPA grants the CRA authority to take various actions to recover amounts owed, including garnishment, property seizure, and requiring third parties to pay amounts due on behalf of the debtor.

The GGPPA imposes various penalties for non-compliance with the fuel charge, including fines for late or incorrect filings, failure to make electronic payments, and registration lapses. Serious infractions, such as making false statements, can lead to criminal charges, with potential penalties including substantial fines or imprisonment, depending on the severity of the offense.

Takeaway

The GGPPA establishes a highly complex framework for carbon pricing in Canada, particularly through its fuel charge. With numerous exemptions, registration requirements, and regulatory intricacies, the GGPPA gives the federal government significant authority to adjust rules and impose compliance measures. Beyond the legal and administrative aspects, the Fuel Charge is a critical component of Canada’s climate change strategy, designed to curb carbon emissions and foster a transition to cleaner energy. For businesses in the fuel supply chain, navigating this law requires careful attention to detail and an understanding of its many provisions. Given the complexity and potential penalties, consulting a professional is crucial for ensuring compliance and taking advantage of applicable exemptions or rebates.

We encourage taxpayers to discuss potential DST questions, implications and or concerns with their Andersen tax advisor.

Andersen Canada Contacts

| Nicolas Rondeau, CPA, Director – Indirect Tax, Andersen Montreal |  | Myriam Vallée, LL.B., M.Fisc. Manager, Andersen Montreal |

Appendix 1

Appendix 1

Registration requirement per type of activity

The following exhibit provides an overview of the registration requirements by type of activity. The GGPPA also allows ministerial discretion to add prescribed persons, prescribed classes of persons or prescribed circumstances that triggers a registration requirement, as well as the possibility to register voluntary or add exclusions from registration.

| Types of registration | |

| Distributor (section 55) | Mandatory: For those producing, importing, delivering marketable/non-marketable natural gas in a listed province or those producing other regulated fuels in a listed province (which includes users of combustible waste). Optional: For those selling, delivering, distributing fuel or removing it from a listed province, under specific circumstances. Restriction: If already registered as an air, marine, or rail carrier (either specified or non-specified) for that fuel type, one cannot register as a distributor for the same fuel. |

| Importer (section 56) | Mandatory: For importing or bringing fuel into a listed province from outside of Canada or from another non-listed province (except for small amounts in a vehicle or under 200 liters of certain fuels). Optional: For certain interjurisdictional rail carriers. Restriction: If already registered as a distributor or as an air, marine, or rail carrier (either specified or non-specified) for that fuel type, one cannot register as an importer for the same fuel. |

| Emitter (section 57) | Optional: For those responsible for covered facilities under the OBPS. |

| User (section 58) | Optional: For using fuel in non-covered activities in a listed province (as long as the person is not already a registered distributor). |

| User of Combustible Waste (section 59) | Mandatory: For those burning combustible waste in a listed province to produce heat or energy. Combustible waste means (a) tires or asphalt shingles whether in whole or in part; or (b) a prescribed substance, material or thing. |

| Air Carrier and Specified Air Carrier (section 60) | Mandatory: For interjurisdictional air carriers (other than registered emitters) using qualifying aviation fuel (e.g. aviation gasoline, aviation turbo fuel). Registration can be either as an air carrier or specified air carrier depending on fuel use during the year. |

| Marine Carrier and Specified Marine Carrier (section 61) | Mandatory: For interjurisdictional marine carriers (other than registered emitters) using qualifying marine fuel (e.g. heavy fuel oil, light fuel oil, marketable natural gas). Registration can be either as a marine carrier or specified marine carrier based on fuel use during the year. |

| Rail Carrier and Specified Rail Carrier (section 62) | Mandatory: For interjurisdictional rail carriers (other than registered emitters) using qualifying rail fuel (e.g. light fuel oil, marketable natural gas). A specified rail carrier registration is required if prescribed by the Fuel Charge Regulations. Currently, three interjurisdictional rail carriers are prescribed: Canadian National Railway Company, Canadian Pacific Railway Company and VIA Rail Canada |

| Road Carrier (section 63) | Mandatory: For interjurisdictional road carriers using qualifying motive fuel (e.g. gasoline, light fuel oil, marketable natural gas, propane) in specified commercial vehicles. A specified commercial vehicle is a vehicle with a minimum weight that is used to provide commercial transportation of individuals or goods by road, and excludes recreational vehicle, including a motor home, bus or pickup truck with attached camper. Restriction: Anyone already registered as a distributor or as an air, marine, or rail carrier (either specified or non-specified) for that type of fuel cannot register as a road carrier. |

Appendix 2

Fuel charge application

The following exhibit provides an overview of the circumstances that trigger the fuel charge.

| Fuel charge application | |

| Delivery (section 17) | Registered distributors delivering fuel in listed provinces must pay the fuel charge, except when delivering to: – a registered distributor, a registered user or a registered specified air, marine or rail carrier in respect of that type of fuel – a registered emitter – a farmer or fisher, if the fuel is gasoline or light fuel oil – a greenhouse operator or remote power plant operator and an exemption certificate applies in respect of the delivery. The exemption certificate must be made in prescribed form containing prescribed information determined by the CRA and must be provided to the supplier prior to the delivery of fuel. For more details visit the following link. According to CRA’s administrative policy, a supplier may not be able to amend a return or claim a rebate of fuel charge remitted by mistake if they receive an exemption certificate after the delivery of the fuel, even if the customer was registered prior to the delivery. |

| Used by a registered Distributor (section 18) | Registered distributors using (burning) fuel must pay the fuel charge unless the fuel is used in a non-covered activity, or if they are also a registered emitter, and the fuel is used in a covered facility. |

| Bringing into a listed province and importation (sections 19-20) | Any person, except registered distributors or specified carriers, bringing or importing fuel into a listed province must pay the fuel charge. For non-registered persons, registered road carrier or registered user of combustible waste, the fuel charge is to be paid and collected by the Canada Border Services Agency under the Customs Act. |

| Production (section 21) | Producers of regulated fuel in listed provinces must pay the fuel charge unless they are registered as a distributor or a registered specified carrier. |

| Diversion from covered facility and diversion by registered user, a farmer, a fisher or a greenhouse operator (section 22-24.1 and Regulations) | The fuel charge can apply when, following a delivery of regulated fuel subject to an exemption certificate, the circumstances allowing for the application of an exemption are not applicable anymore. |

| Combustible waste (section 25) | Anyone burning combustible waste to produce heat or energy in a listed province must pay the fuel charge. |

| Application of the fuel charge to Air, Marine, Rail and Road Carriers (specified and non-specified) (sections 28-34) | Under the GGPPA, registered carriers must calculate their fuel charge based on the net fuel quantity for a given reporting period, tied to the specific regulated fuel type and the listed province in which the fuel is used. This process varies depending on the mode of transport, with specific rules for each registration type, including an annual net fuel adjustment for rail carriers (due to their net fuel quantity of each reporting period being an estimate). If the net fuel quantity or the annual net fuel adjustment is a negative amount, the person must receive a rebate. Again, the GGPPA grants the federal government significant regulatory authority to introduce or modify elements in the net fuel calculation. |

| Regulation (section 26-27) | The GGPPA allows for a large discretion to add by regulation prescribed circumstances triggering the application of the fuel charge, or an exemption from the fuel charge. |

| Ceasing to be registered (section 39) | If a person holds a quantity of a type of fuel in a listed province at the time, were it ceases to be registered as a distributor or a specified air, marine or rail carrier in respect of that type of fuel, the person must pay the fuel charge in respect of the fuel and the listed province except if the person is a registered emitter at the particular time to the extent that the fuel is held by the person at, or is in transit to, a covered facility of the person. |

[1] Click here to visit Schedule 2. Click here to see the trajectory of the rates for each regulated fuel and combustible waste from April 1, 2023, to April 1, 2030.