B.C. Provincial Budget Tax Updates 2025-2026

Overview

On March 4th, 2025, the B.C. government announced changes to its provincial tax laws in its budget 2025 Standing Strong for B.C. This comprehensive summary highlights the key changes that will influence the provincial tax environment in the coming years.

Personal Income Taxes Measures

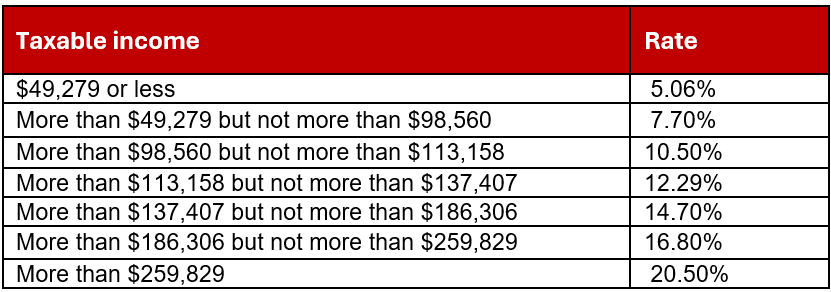

The budget introduces no change to the personal income tax rates. The income tax rates for the 2025 taxation year, based on your taxable income, are as follows:

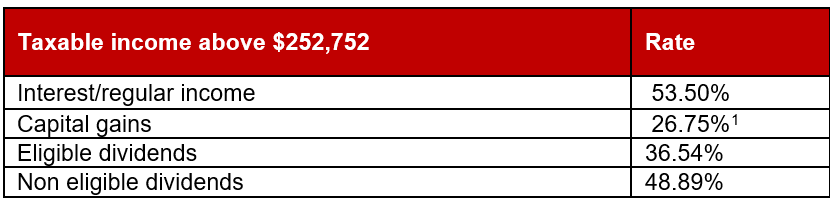

The current personal combined income tax rates for top marginal tax rate in 2025 are outlined below:

BC Family Benefit Enhancement

Starting January 1, 2025, grieving families will continue receiving the BC Family Benefit for six months after a child’s passing. This change aligns with recent federal modifications to child benefit programs.

Small Business Venture Capital Tax Credit Increase

Effective for 2025 and subsequent taxation years, the annual credit limit that an individual can claim for investments made on or after March 4, 2025, is increased from $120,000 to $300,000.

Corporate Income Taxes Measures

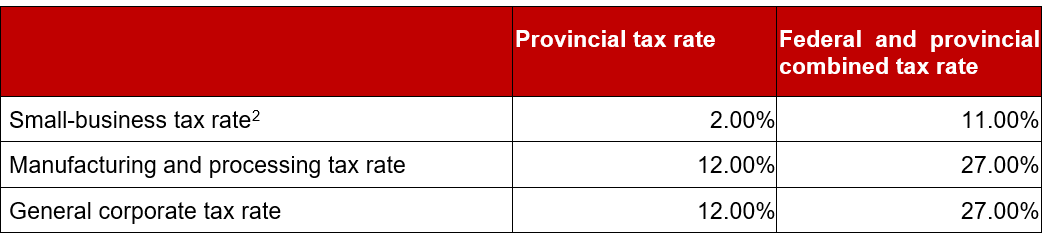

There are no proposed changes to corporate income tax rates or the $500,000 small-business limit for 2025. The corporate income tax rates for British-Colombia in 2025 are as follows:

Interactive Digital Media Tax Credit Increase

The tax credit for companies developing interactive digital media products will increase from 17.5% to 25%, effective September 1, 2025. The credit will also be permanently implemented, providing long-term planning certainty for companies in the sector.

Clean Buildings Tax Credit Extension

The deadline for qualifying expenditures for the clean buildings tax credit is extended by one year to March 31, 2026.

Training Tax Credit for Apprentices Extension

The apprenticeship tax credit, originally set to expire on December 31, 2025, is now extended to December 31, 2028. Notably, the enhanced credits for First Nations individuals and apprentices with disabilities will remain in place, even after the federal Apprenticeship Incentive Grant expires on March 31, 2025.

Film & Television Tax Incentives:

- The basic Film Incentive BC tax credit, which applies to domestic productions, will increase from 35% to 40% of eligible labor costs, while the Production Services Tax Credit, benefiting international productions, rises from 28% to 36% for productions commencing after January 1, 2025.

- Starting January 1, 2025, animation productions set in regional or distant locations can qualify for regional and distant location tax credits, provided they maintain a physical office with a workforce who is physically present and working there at least 50 per cent of the time.

- Effective January 1, 2025, a new Major Production Tax Credit will be available for high-budget productions with production costs greater than $200 million. It will be equal to 2% of a corporation’s accredited qualified BC labour expenditures in respect of the major production.

Small Business Venture Capital Program Budget Increase

From 2025 to 2027, the total annual amount of tax credits that may be approved under the small business venture capital program is temporarily increased by $15 million to $53.5 million. Of this, $10 million is evenly allocated to investment streams for new businesses, clean technology, interactive digital media, and businesses outside Metro Vancouver and the Capital region, while $5 million is available for all eligible businesses.

New Mine Allowance Extension

The New Mine Allowance, which permits mining companies to claim an accelerated deduction for capital expenditures, is extended to the end of 2030.

Sales Tax Measures

Provincial Sales Tax (PST) on Used Zero-Emission Vehicles

As of May 1, 2025, the exemption on PST for used electric vehicles will be eliminated.

Other Tax Measures

Property Tax Exemptions for First Nations

- As of May 21, 2024, certain property transfers among First Nations under the federal Indian Act will be exempt from the Property Transfer Tax.

- Starting in 2026, eligible First Nations properties used for cultural, or community purposes will be exempt from annual provincial school and rural property taxes, further supporting Indigenous communities.

- Starting in the 2026 taxation year, property tax will no longer apply to lands and improvements in rural areas within a treaty-designated foreshore area if they are owned or held by the Modern Treaty First Nation or its public institutions.

Speculation & Vacancy Tax Rate Increase

Effective January 1, 2026, the tax rate of the Speculation and Vacancy Tax will double from 0.5% to 1% for Canadian citizens and permanent-resident owners, while foreign owners and untaxed worldwide earners will see an increase from 2% to 3%. This increase is intended to encourage property availability for residents rather than investors leaving units vacant. To mitigate the impact of this increase on B.C. residents, the non-refundable speculation and vacancy tax credit available to local homeowners will increase from $2,000 to $4,000.

Additionally, effective retroactively to January 1, 2024, the Predator Ridge resort in the City of Vernon is excluded from the specified area for the speculation and vacancy tax.

Carbon Tax

The scheduled increase in carbon tax by $15 per ton on April 1, 2025, will, under BC’s budget, proceed as planned. However, the provincial government remains committed to removing the consumer carbon tax should the federal government remove the requirement for carbon pricing across Canada (also known as the federal backstop). As it stands, 100 per cent of incremental carbon tax revenue is returned to British Columbians through the climate action tax credit.

As expected, on March 22, 2025, the Federal government made regulations that ceased the application of the federal fuel charge and in turn announced that it was removing the provincial requirements relating to the consumer carbon tax, effective as of April 1st, 2025. Following this announcement, the B.C. government passed legislation to eliminate the B.C. carbon tax effective as well, on April 1, 2025.

The budget also includes various technical and administrative changes.

For further information, visit https://www.bcbudget.gov.bc.ca/2025/default.htm

[1] Based on the current 50% capital gain inclusion rate in effect under the current Federal legislation.

[2] Applies to the first $500,000 of active taxable income of Canadian-Controlled Private Corporations (CCPCs).