Manitoba Provincial Budget Tax Updates 2025-2026

Overview

On March 20th, 2025, Manitoba’s Finance Minister presented the province’s 2025 budget “Building One Manitoba”, which projects deficits of $794 million for 2025-26 and $327 million for 2026-27.

Personal Income Tax Measures

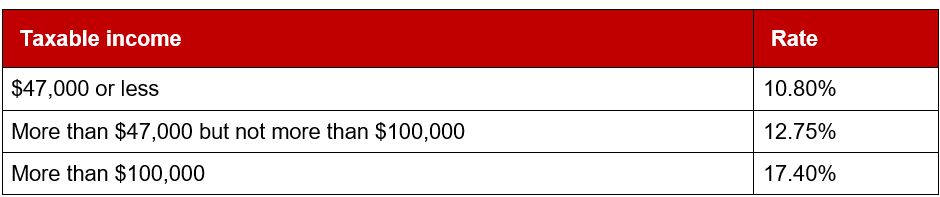

The income tax rates for the 2025 taxation year, based on your taxable income, are as follows:

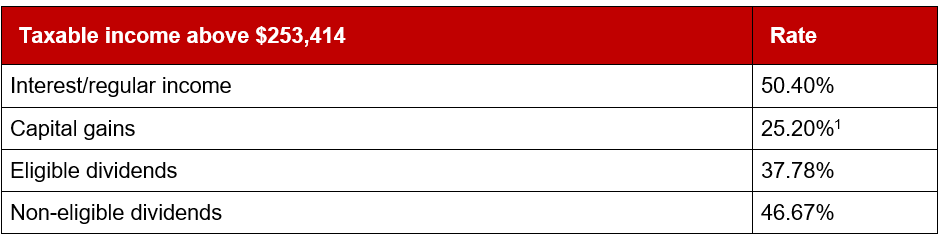

The current personal combined income tax rates for top marginal tax rate in 2024 are outlined below:

Freezing of the Basic Personal Amount (BPA) and tax bracket thresholds

Beginning with the 2025 tax year, indexation of the BPA and tax bracket thresholds to inflation will be frozen. The BPA was $15,780 for 2024.

Increase of the Renters Affordability Tax Credit

In the 2025 tax year, the maximum annual Renters Affordability Tax Credit would be $575, and the maximum seniors’ top-up by $28, from $300 to $328, for the 2025 tax year.

For the 2026 tax year, the maximum Renters Affordability Tax Credit will rise to $625, and the senior citizens’ top-up will increase to a maximum of $357.

Increase of the Volunteer Firefighter and Search and Rescue Amount

In the 2025 tax year, the Volunteer Firefighter and Search and Rescue Amount will be increased from $3,000 to $6,000, raising the maximum annual credit value to $648.

Increase of the Homeowners Affordability Tax Credit

For the 2026 property tax year, the maximum Homeowners Affordability Tax Credit will be increased by $100, from $1,500 to $1,600.

Homeowners with gross school tax bills exceeding $1,500 in 2026 will benefit from this increase, as the credit will now cover up to an additional $100 of their school taxes.

Fully funded by the Manitoba government through general revenues, the Homeowners Affordability Tax Credit does not affect school funding.

Corporate Income Tax Measures

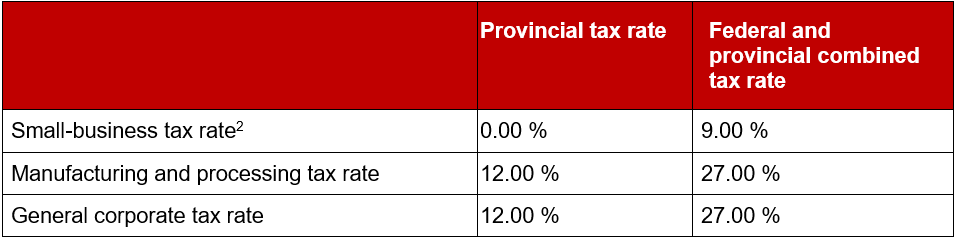

There are no proposed changes to corporate income tax rates or the $500,000 small-business limit for 2025.

The corporate income tax rates for Manitoba in 2025 are as follows:

Abolitions of the Corporation Capital Tax Act

Effective for fiscal years beginning after March 31, 2025, the corporation capital tax paid by crown corporations is eliminated.

Cultural Industries Printing Tax Credit made permanent

The Cultural Industries Printing Tax Credit, which offers eligible businesses a 35% refundable tax credit on salaries and wages paid to Manitoba employees, will be made permanent, instead of expiring on December 31, 2024.

Technical adjustments to the Mining Tax Act

The following technical adjustments will be introduced:

- Repealing the new investment tax credit, which is now obsolete as it only applied to investments made before January 1, 2004.

- The requirement for the Minister of Finance to designate a new mine or major expansion will be removed.

- The special tax rate of 0.5 percent, which is applied in addition to regular tax rates on mining operators’ profits, will be eliminated. Currently, this tax is paid but refunded to mining operators.

Changes to the Health and Post Secondary Education Tax Levy

Starting January 1, 2026, the exemption threshold will increase from $2.25 million to $2.5 million in annual remuneration. Additionally, the threshold for businesses to pay a reduced effective rate will be raised from $4.5 million to $5 million.

Sales Tax measures

Application of the retail sales tax to cloud Computing

Beginning January 1, 2026, retail sales tax will be applied to cloud computing services, including software subscriptions, data storage, and remote computer processing. This change is due to technological advancements in the industry.

Retail Sales Tax and Tobacco Tax Registration Registry

In 2025, Manitoba Finance will launch an online service allowing taxpayers to check whether a business is registered for retail sales tax. A similar registry will also be created for tobacco tax.

Other Tax Measures

Administrative changes to the Income Tax Act

Changes are made to:

- Exclude trusts from eligibility for the Family Tax Benefit.

- Align the eligibility timing for the Seniors School Tax Rebate with the Homeowners Affordability Tax Credit.

Penalty and interest waivers under the Tax Administration and Miscellaneous Taxes Act

The reporting requirements for penalty and interest waivers granted to taxpayers will be simplified.

Preventing Avoidance of Land Transfer Tax Through Use of Certain Ownership Structures

The current provisions in The Tax Administration and Miscellaneous Taxes Act do not require the payment of land transfer taxes when there is an unregistered change in the beneficial ownership of land. To enhance tax fairness, the government will consider legislative changes aimed at preventing the avoidance of land transfer tax through legal structures that separate legal and beneficial ownership of property.

Tobacco Band Assessment Agreements

The Tobacco Band Assessment program allows First Nations to generate own-source revenue for community investments. Under this program, participating First Nations enter into agreements with the Province of Manitoba to apply a tobacco band assessment equal to the provincial tobacco tax rate on tobacco sales to First Nations purchasers. These agreements are being revised to extend their duration from five years to ten years and to lower the administration fee from 1.0% to 0.25%.

[1] Based on the current 50% capital gain inclusion rate in effect under the current Federal legislation.

[2] Applies to the first $500,000 of active taxable income of Canadian-Controlled Private Corporations (CCPCs).